Over the past five years, Braskem has moved through three distinct macro regimes: the COVID shock, the 2022 cost inflation cycle, and the current geopolitical volatility phase.

At first glance, these periods appear fundamentally different. In reality, they are variations of the same mechanism:

naphtha drives costs, polymers follow with a lag, and spreads determine everything.

Today, however, both management commentary and Braskem stock suggest a level of pessimism that appears disconnected from observable polymer prices—particularly when compared to 2022.

Part 1. The COVID Shock: When Deleveraging Was Not What It Seemed

The onset of the COVID-19 created a highly asymmetric shock across the petrochemical value chain, and Braskem was a clear beneficiary—at least at the EBITDA level.

However, a closer look at 2020 suggests that the company’s rapid deleveraging was driven less by structural balance sheet improvement and more by a temporary dislocation between feedstock costs, product pricing, and working capital dynamics.

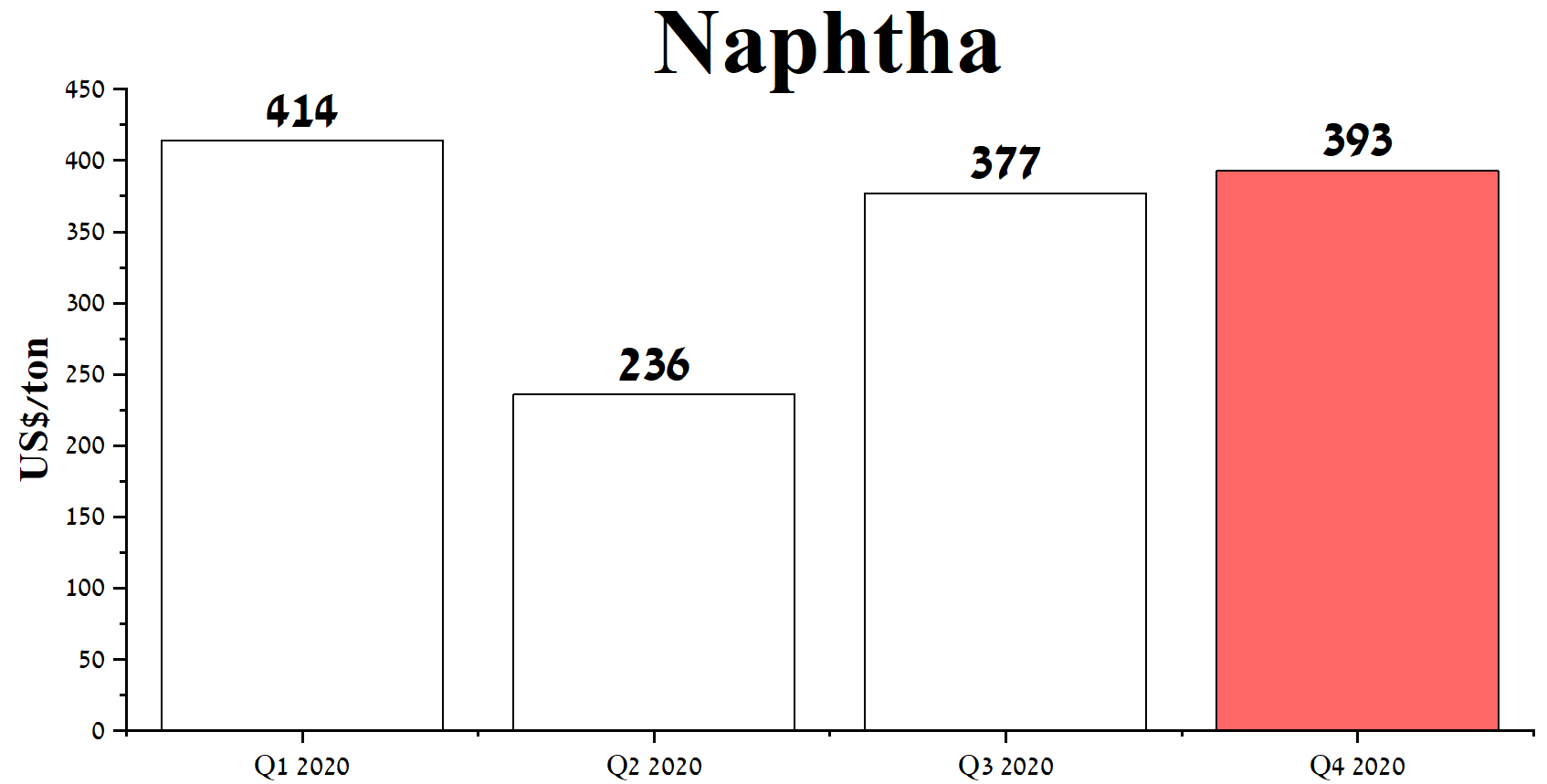

In Q1 2020, naphtha prices hovered around $414/ton, reflecting the lagged impact of collapsing oil demand.

By Q2 2020, prices had fallen sharply to approximately $236/ton, implying a ~43% sequential decline.

In the 3rd quarter its price rose to $377/ton as I indicated in the chart below.

Source: graph was made by Author based on the financial reports of Braskem [Brazil]

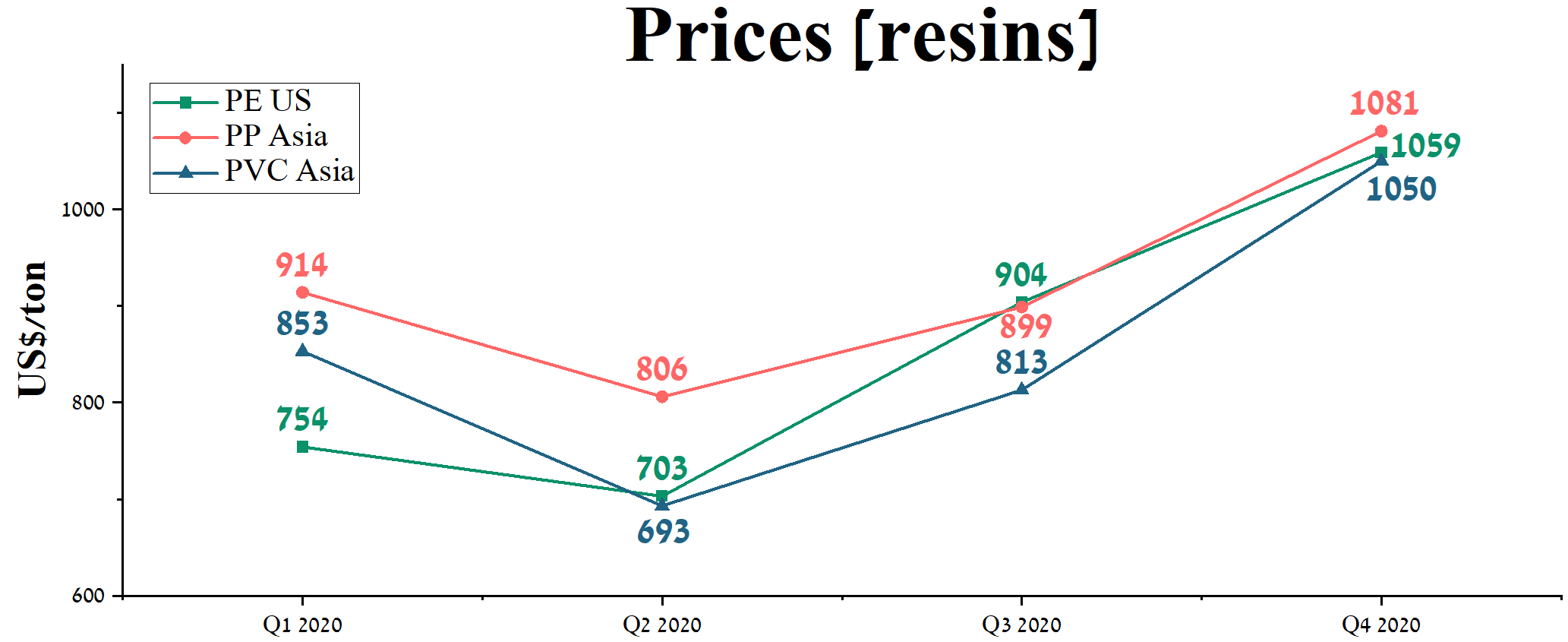

At the same time, downstream polymer prices remained relatively stable.

I must note that from now on and in this part of the article, I will only discuss the second and third quarters of 2020.

Polypropylene Asia: ~$806 → $899

Polyethylene U.S.: ~$703 → $904

Polyvinyl Asia: ~$693 → $813

Source: graph was made by Author based on the financial reports of Braskem [Brazil]

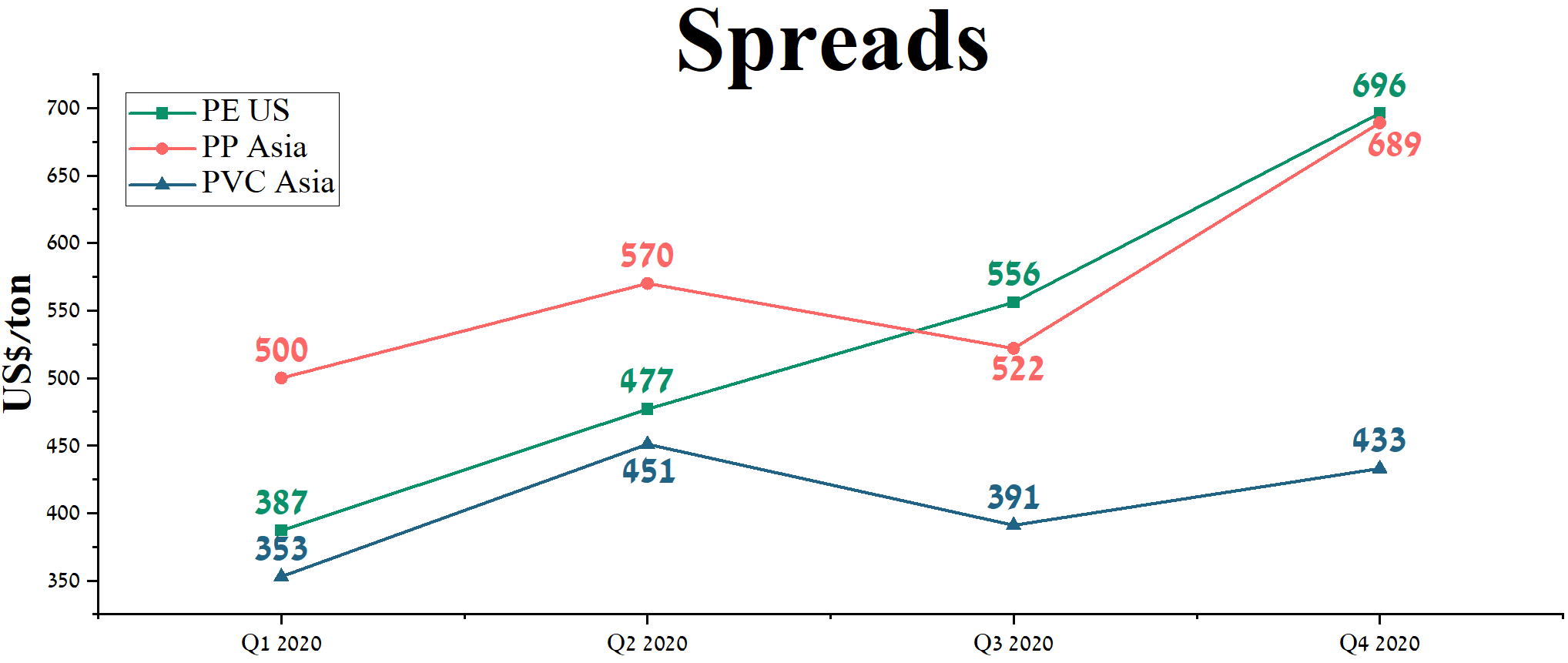

This divergence led to a rapid expansion in spreads, particularly in polyethylene, which translated almost mechanically into higher profitability.

Source: graph was made by Author based on the financial reports of Braskem [Brazil]

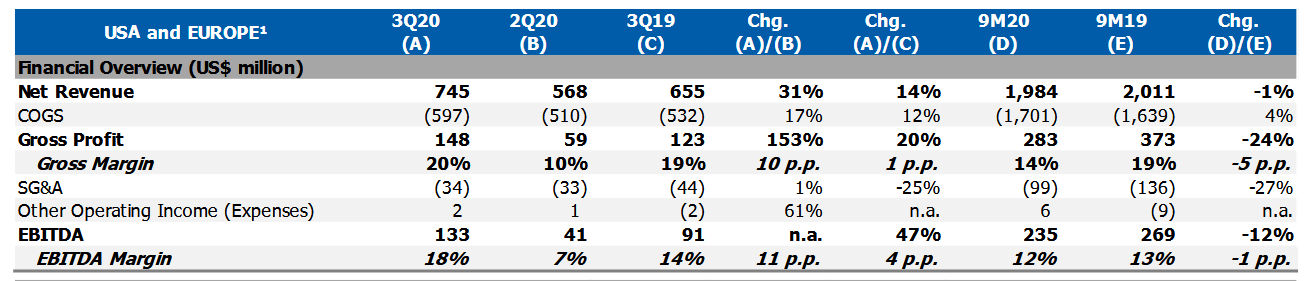

The impact on earnings was immediate. EBITDA in Brazil increased from $219 million in 2Q20 to $529 million in 3Q20 (+148% QoQ), while the United States and Europe segment rose from $45 million to $133 million (+223% QoQ).

Source: Braskem

The recovery was supported by both improved margins and a normalization in operating rates, with Brazilian utilization reaching 87% (+17 p.p. QoQ).

At the headline level, this translated into rapid deleveraging. Net debt remained broadly stable, but the surge in EBITDA drove net debt-to-EBITDA from above 7x to below 5x within a single quarter, creating the impression of a structurally improving balance sheet.

Source: Braskem

Management Commentary

Despite this apparent improvement, a critical offsetting force was developing beneath the surface—one tied directly to feedstock sourcing.

Historically, Braskem relied heavily on imported naphtha, not only for cost optimization but also for financing flexibility. International suppliers typically offered extended payment terms, allowing the company to delay cash outflows and support working capital. In 2020, this model shifted following a commercial agreement with Petrobras.

As a result, Braskem increased domestic purchases to approximately two-thirds of total naphtha consumption. While the agreement included a meaningful discount of $15–35 per ton, it fundamentally altered cash flow dynamics.

When we import, we are able to have extended payment terms from our suppliers. So we have in working capital a good volume coming from this imported naphtha purchase.

And a lot of that naphtha is being paid or was paid in the 1H of this year. Now this year, it is a reverse. We are buying roughly 2/3 of our naphtha from Petrobras.

And because of that with Petrobras, we do not have the extended payment terms. So in the end, looking at cash flow, we are paying naphtha from last year and we are also paying naphtha for this year from the purchases from Petrobras.

The timing of this transition amplified its impact. During the first half of 2020, the company was simultaneously settling deferred payments related to imported naphtha while also paying for current Petrobras volumes on a much shorter cycle. This created a double cash outflow, which offset much of the EBITDA-driven improvement.

That is why you will see the draw on cash from working capital. Moving forward, and looking at the 2H20, we will continue prioritizing the purchases of naphtha according to market dynamics.

Because the naphtha price is holding up in the 2H20, I would think that the usual situation is that we would increase import a little bit.”

Interim conclusion

The key takeaway is not the strength of the recovery itself, but its composition. Braskem’s deleveraging during this period was driven primarily by a denominator effect—EBITDA expansion—rather than a fundamental improvement in cash generation.

This created a temporary disconnect between profitability and liquidity, where margins improved sharply but cash flow lagged due to adverse working capital dynamics.

Part 2. 2022: Geopolitics, Cost Inflation, and the Limits of Resilience

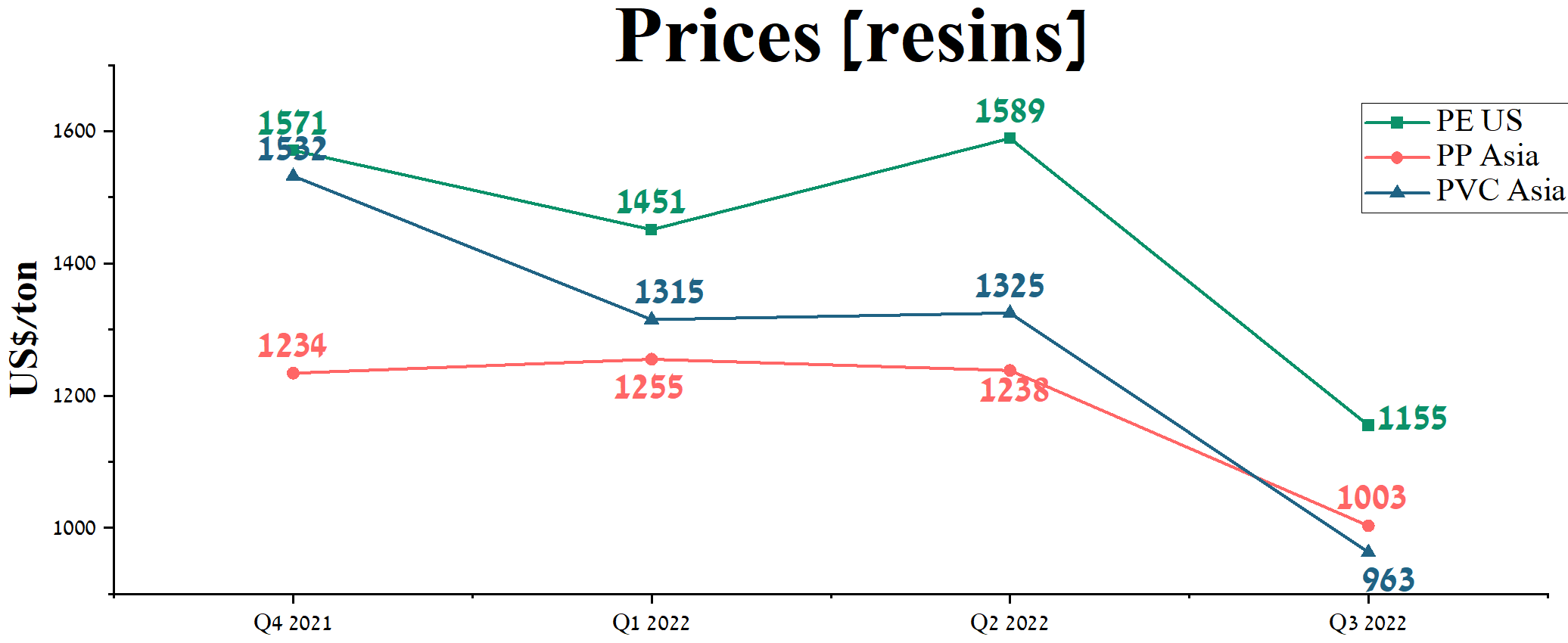

The first quarter of 2022 marked a turning point for the petrochemical cycle. While headline polymer prices remained elevated—at levels comparable to those seen in late 2025 in China—the underlying economics for Braskem deteriorated materially.

Source: graph was made by Author based on the financial reports of Braskem [Brazil]

The key difference from 2020 was not pricing, but cost pressure.

Naphtha prices surged to approximately $884/ton in 1Q22, more than 3x from the trough levels observed in 2Q20. At the same time, polymer prices remained relatively strong:

Polypropylene Asia: ~$806 → $899

Polyethylene U.S.: ~$703 → $904

Polyvinyl Asia: ~$693 → $813

Source: graph was made by Author based on the financial reports of Braskem [Brazil]

At first glance, this pricing environment appeared supportive. However, unlike the COVID dislocation—where falling feedstock costs expanded margins—2022 was defined by input cost inflation outpacing downstream pricing, resulting in a sharp compression of spreads.

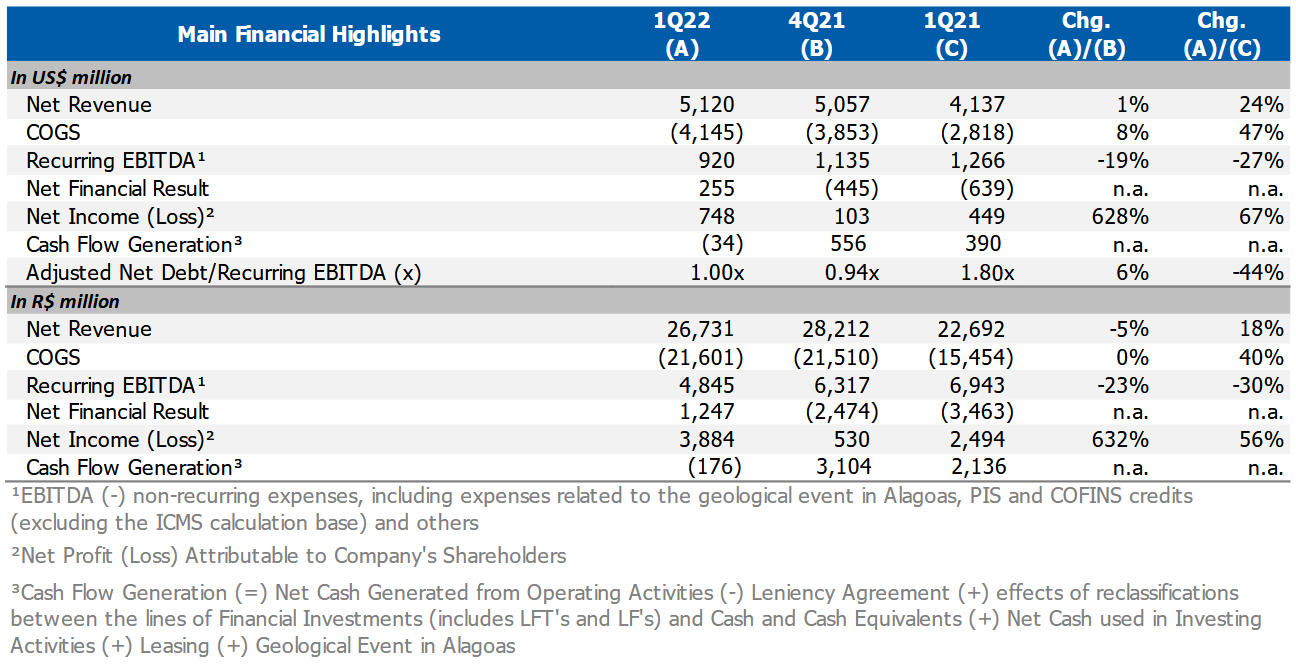

This shift was directly reflected in financial performance. Braskem reported Recurring EBITDA of $920 million in 1Q22, down 19% sequentially and 27% year-over-year, despite still-elevated polymer prices. The decline was primarily driven by the normalization—and in many cases compression—of spreads across key products and regions.

Source: Braskem

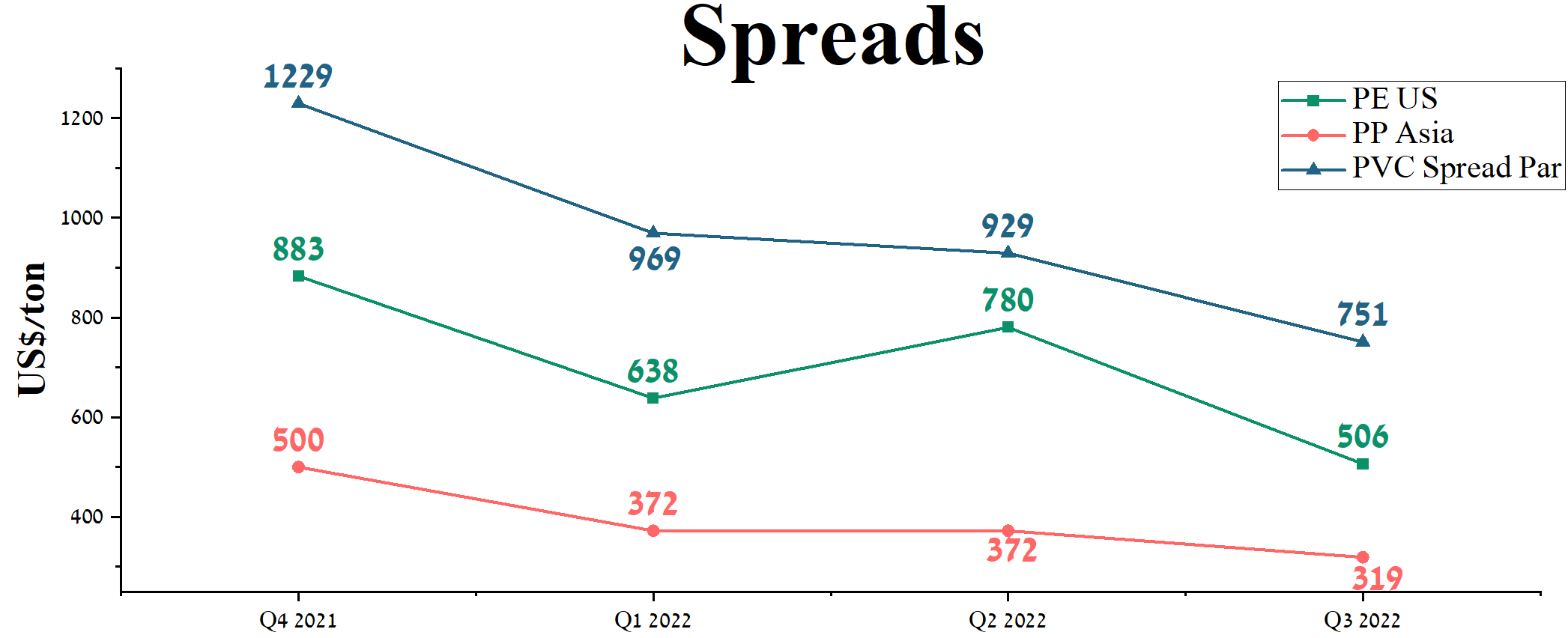

Spread Compression Across the Portfolio

The deterioration was broad-based and structurally different from the demand-driven weakness seen in 2020:

PE spreads in Brazil declined 28% QoQ, as rising naphtha prices offset stable demand

PP spreads contracted 26% QoQ, reflecting higher feedstock costs and weaker Asian demand

PVC spreads fell 21% QoQ, driven by lower prices and rising input costs

In the U.S. and Europe, the pattern was similar. Even where demand remained relatively healthy, margin pressure emerged due to cost inflation and normalization of supply conditions following earlier disruptions such as Winter Storm Uri.

Management Commentary (1Q22 Call)

“The beginning of 2022 was marked by geopolitical tensions, which brought a lot of volatility to the petrochemical scenario.”

“the expectation of external consultants for the PE naphtha spreads for 2022 is already at a level above the pre-war Russia and Ukraine.”

“for the remaining quarters of this year, PE naphtha spreads are expected to remain at healthy levels and above the recent historical average”

Despite this relatively constructive forward-looking tone, the actual quarterly data suggests that “healthy” spreads were already under pressure in real time, particularly when compared to the extraordinary levels seen in 2021.

Interim conclusion

If 2020 demonstrated how quickly EBITDA can expand when feedstock costs collapse, 2022 showed the opposite: how rapidly profitability can erode when costs rise faster than prices.

Braskem entered 2022 with a more diversified and theoretically resilient operating model. However, the quarter made clear that diversification can mitigate—but not eliminate—exposure to global commodity cycles.

The key distinction relative to 2020 is critical:

2020: Falling costs → expanding spreads → EBITDA-driven deleveraging

2022: Rising costs → compressing spreads → EBITDA contraction despite high prices

This shift underscores a recurring theme in Braskem’s financial profile:

headline pricing is a poor proxy for profitability.

Part 3. 2026: Geopolitics, Structural Pressure, and a Mispriced Cycle

The first quarter of 2026 once again places Braskem at the intersection of geopolitics and petrochemical cycles. However, unlike both 2020 and 2022, the current environment combines elements of both phases—rising feedstock costs and tightening supply—while the equity market reflects a far more pessimistic view.

Naphtha prices averaged around $760/ton in 1Q26, rising to approximately $850+/ton by the end of March, driven by escalating tensions in the Middle East.

Source: TRADING ECONOMICS

At the same time, polymer prices in China [largest chemicals manufacturer in the world] have been moving higher, albeit with a lag:

Polypropylene (PP): ~8,100 → 9,184 CNY/t ($1,157 → $1,312)

Polyethylene (PE): ~8,000 → 8,693 CNY/t ($1,142 → $1,241)

TRADING ECONOMICS

This lagged transmission mechanism—where feedstock costs adjust first and polymer prices follow—remains a defining feature of the petrochemical cycle. In the short term, it compresses margins; only later does pricing catch up, partially restoring spreads.

Geopolitical Shock: Supply Risk, Not Demand Collapse

The current volatility is being driven not by demand destruction, but by supply-side risks linked to the Middle East.

Management Commentary (4Q25 Call)

“we have observed an escalation of tensions in the Middle East involving the United States Israel and Iran… reflected in greater volatility in commodity prices, especially Brent crude oil and naphtha”

“Naphtha has followed this volatility given its direct link to oil, which can impact the costs of the petrochemical chain”

“lower availability of feedstock imported from the Middle East… could lead to shutdowns and production reductions”

“a scenario of lower global supply could lead to an increase in operating rates to meet the shortage of resins”

A key risk factor remains the potential disruption of the Strait of Hormuz, which is critical for global petrochemical flows. Management estimates that a severe restriction scenario could reduce global polyethylene supply by 6–19 million tons (4–11%) and polypropylene by 7–10 million tons (4–5%).

This introduces a dynamic not seen in 2020 or 2022:

simultaneous cost inflation and potential supply tightening, which could eventually support prices—but only after an initial margin squeeze.

Industry Backdrop: Weak Utilization, Fragile Demand

Despite rising prices, the industry enters this phase from a position of structural weakness.

Cycle Pressure (Key Quote)

“the prolonged petrochemical downcycle has resulted in lowest industry operating rates in decades… 79% for polyethylene and 74% for polypropylene”

Global demand for polyethylene and polypropylene declined by approximately 3 million tons, reflecting weaker consumption across key regions. This means that, unlike 2020, higher prices are not being driven by strong demand, but rather by cost push and supply constraints.

Feedstock Strategy: Reduced Risk, Not Eliminated Exposure

One of the most important structural changes since 2020 is Braskem’s gradual reduction in naphtha dependency.

Strategic Direction (Key Quotes)

“today, we are 80% naphtha-based… and our plan is, by 2030, to reach 60% naphtha and 40% ethanol and gas”

“we’re also importing ethane from the U.S… as a way of sidestepping the increasing cost of feedstocks”

This diversification is already visible across regions:

Brazil: partial shift toward ethane and propane

U.S.: structurally advantaged gas-based operations

Mexico (Braskem Idesa):

predominantly ethane-based

minimal direct exposure to naphtha

Operational data confirms this shift. In 4Q25, Braskem Idesa increased ethane supply to ~29.4 kb/d (imports), alongside 15.9 kb/d from Pemex and additional Fast Track volumes. This supported higher utilization rates and reinforces the structural advantage of gas-based production.

Sourcing Advantage: Relative, Not Absolute

Unlike Asian competitors, Braskem’s feedstock supply is not structurally constrained.

Sourcing Commentary

“our main supplier of naphtha is the U.S… the U.S. has a surplus of naphtha supply”

“with regard to our naphtha supply… it is not impacted by any of these conflicts”

“of course, there is an impact in higher prices”

This creates a relative advantage versus Asian producers dependent on Middle Eastern supply, some of whom are already reducing operating rates. However, the benefit is price-based rather than cost-based—Braskem still pays higher global prices, even if supply is secure.

Pricing Actions: Cost Pass-Through Under Constraints

Recent commercial actions highlight the current environment. In Brazil, Braskem implemented a R$6,500/ton increase in polyethylene prices, combined with strict volume caps (initially ~35% of demand).

Valuation Disconnect: 2022 vs 2026

Perhaps the most striking feature of the current setup is the divergence between fundamentals and equity pricing.

1Q22:

Polymer prices: ~$1,350–1,380/t

Naphtha: ~$950/t

Stock: ~$18

1Q26:

Polymer prices: ~$1,200–1,350/t (now rising above 2022 levels)

Naphtha: ~$760–850/t

Stock: ~$3.5

Despite a broadly similar pricing environment—and in some cases higher polymer prices—the stock trades at a fraction of its 2022 level.

Conclusion: A Cycle Misread

Across all three periods, one principle holds:

Margins are driven not by absolute prices, but by the timing between feedstock and polymer pricing.

Today, the market appears to be extrapolating short-term cost pressure while ignoring:

stabilization in naphtha (~$820–850)

continued recovery in polymer prices

lagged margin expansion potential

structural diversification away from naphtha

At the same time, management commentary remains heavily focused on downside risks—geopolitics, logistics, and volatility—despite a setup that is fundamentally less severe than 2022.

The result is a rare alignment:

cycle improving (with lag)

management cautious

equity deeply discounted

In this context, Braskem is not simply a leveraged petrochemical company under pressure.

It is a case where:

the cycle, the narrative, and the valuation are no longer aligned.

Disclaimer

The information provided in this publication is for informational and educational purposes only and should not be construed as financial, investment, legal, or tax advice. The views and opinions expressed are solely those of the author and are based on publicly available information believed to be reliable, but their accuracy and completeness cannot be guaranteed.

Nothing in this publication constitutes a recommendation, solicitation, or offer to buy or sell any securities, commodities, or financial instruments. Readers should conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.

The author may hold positions in companies or assets mentioned in this publication and may change these positions at any time without notice. Past performance and historical trends are not reliable indicators of future results.

By reading this publication, you agree that the author and ALLKA Research shall not be held liable for any direct or indirect losses resulting from the use of the information contained herein.

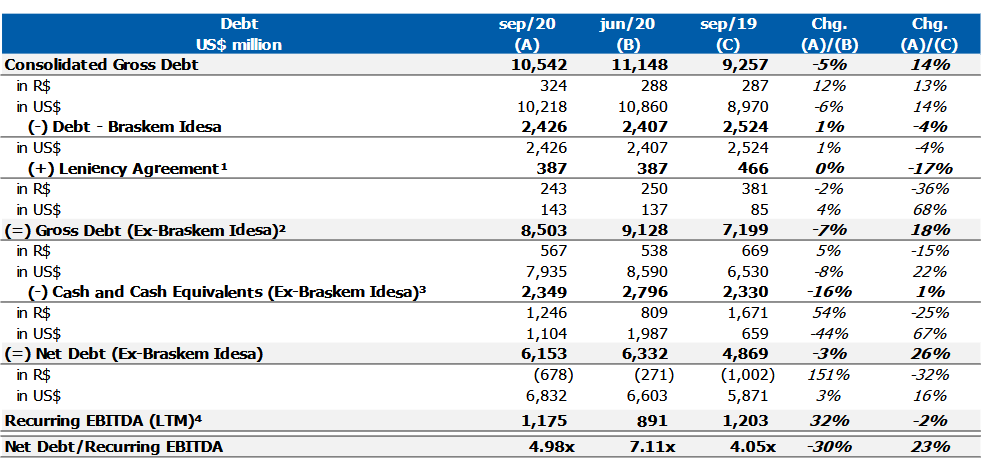

Thoughts on the debt situation?