Braskem Bets on LPG Feedstock Shift as Polymer Prices Rebound

Braskem is accelerating efforts to improve its cost structure and reposition its petrochemical portfolio as the global polymer market begins to stabilize after a prolonged downcycle.

The Brazilian producer is advancing several strategic initiatives aimed at reducing feedstock costs, increasing operational flexibility, and improving profitability across its integrated petrochemical system.

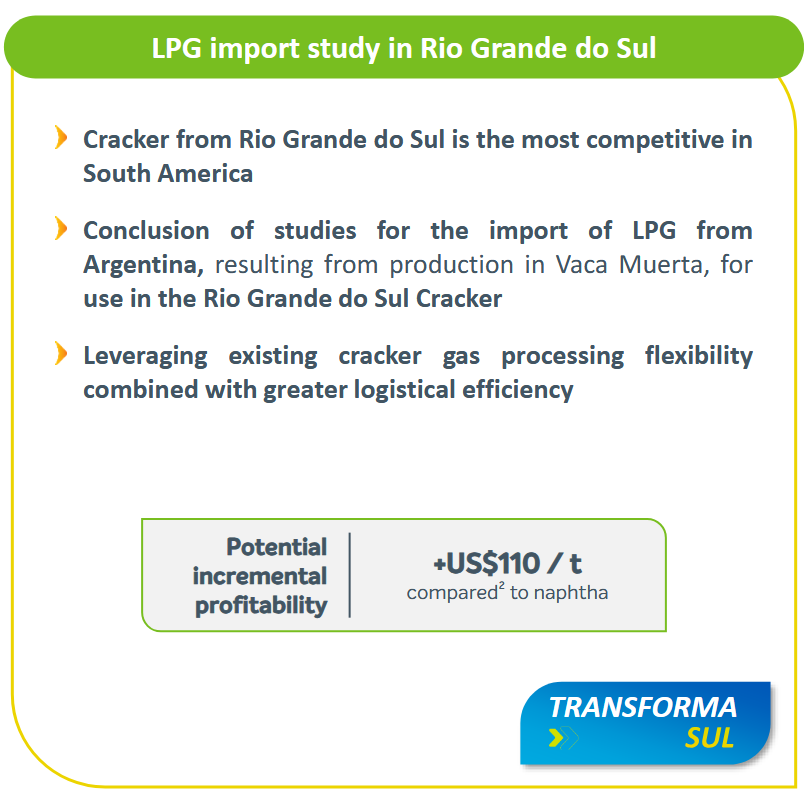

One of the most notable developments is the completion of a study under the Transforma Sul initiative evaluating the import of LPG from Argentina to supply the company’s petrochemical complex in southern Brazil.

LPG imports could materially improve margins

Management confirmed that the study assessed the feasibility of importing LPG produced in Argentina’s prolific Vaca Muerta formation and using it as feedstock at the company’s petrochemical complex in Rio Grande do Sul.

According to Braskem, the Rio Grande do Sul cracker is already the most competitive naphtha-based petrochemical plant in South America and sits among the lowest-cost producers globally on the ethylene cash cost curve.

The LPG import initiative is designed to leverage the plant’s existing gas-processing flexibility, allowing it to partially substitute naphtha with LPG feedstock.

If implemented, the strategy could generate incremental profitability of approximately $110 per ton compared with the continued use of naphtha.

Source: Braskem

The economics are driven by several structural advantages:

• Lower feedstock costs from Argentina’s rapidly growing shale production

• Improved logistical efficiency due to geographic proximity

• Higher olefin yields typically associated with lighter feedstocks such as LPG

Argentina’s Vaca Muerta shale play has emerged as one of the fastest-growing unconventional hydrocarbon developments globally, producing increasing volumes of propane and butane that are seeking export markets across South America.

By tapping this supply, Braskem could reduce its exposure to volatile global naphtha prices, which are closely tied to crude oil benchmarks.

Management described the initiative as part of a broader effort to “modify operations to ensure efficiency, flexibility, and long-term sustainability.”

A broader feedstock transition strategy

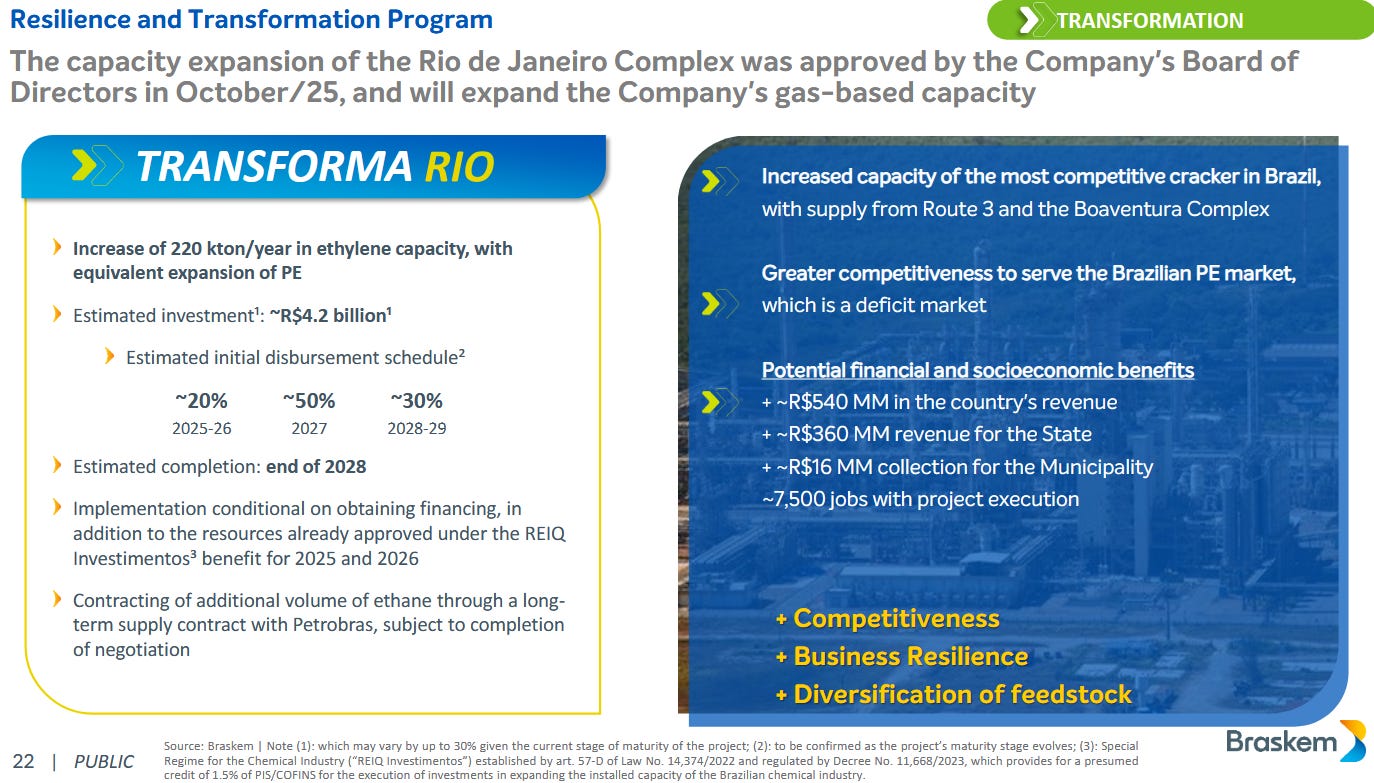

The LPG import study forms part of a wider transformation program that includes the Transforma Rio project.

Under this initiative, Braskem’s board approved the expansion of its petrochemical complex in Rio de Janeiro in October 2025.

The project will add:

• 220 thousand tons per year of ethylene capacity

• A corresponding expansion in polyethylene production

• A larger share of gas-based feedstocks in the company’s raw material mix

Total investment is estimated at R$4.2 billion, with completion targeted for late 2028.

Source: Braskem

The expansion reflects a structural shift underway across the global petrochemical industry, where producers are increasingly seeking to move away from oil-derived feedstocks toward natural gas liquids and LPG, which offer significantly lower production costs.

Polymer markets show signs of recovery

The timing of Braskem’s strategic repositioning coincides with a notable recovery in polymer prices in China, the world’s largest plastics market.

China accounts for roughly 30% of global plastics production, making its domestic pricing trends a critical indicator for the entire petrochemical value chain.

Recent market data show a sharp rebound in several key polymers:

• Polyvinyl chloride: 5,749 CNY per ton ($836.95)

• Polyethylene: 8,391 CNY per ton ($1,221.58)

• Polypropylene: 8,505 CNY per ton ($1,238.17)

Source:

Polyethylene prices have risen more than 23% over the past month, suggesting that the prolonged oversupply cycle that weighed on the global polymer industry through 2023–2025 may be starting to ease.

Supply disruptions tightening the market

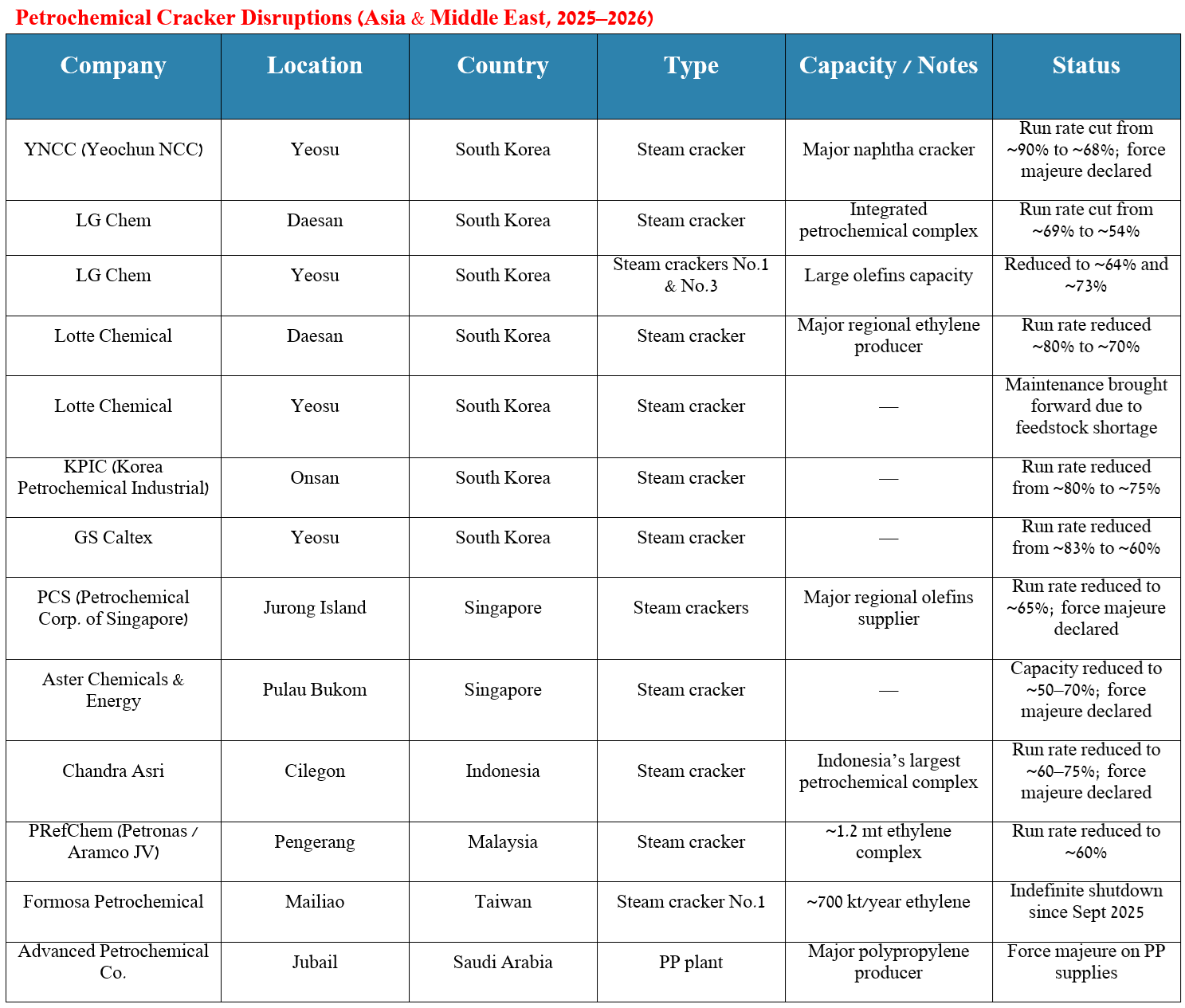

Another factor supporting the recent recovery in polymer prices is a growing number of cracker shutdowns across the Middle East and Asia.

Several petrochemical facilities in these regions have reduced operating rates or temporarily halted production amid weak margins and high feedstock costs earlier in the cycle.

Because petrochemical crackers require complex restart procedures—including catalyst replacement and system stabilization—many plants cannot immediately return to full capacity even if market conditions improve.

This dynamic can tighten global polymer supply more rapidly than expected once demand begins to recover.

Source: table was made by Author

In addition, logistical disruptions linked to geopolitical tensions in the Middle East have complicated feedstock flows and delayed shipments of petrochemical derivatives to Asian markets.

For global producers such as Braskem, these supply constraints could accelerate the normalization of industry margins.

Strategic implications

Taken together, the feedstock transition initiatives and the improving polymer price environment could significantly strengthen Braskem’s earnings trajectory.

A potential $110 per ton margin improvement from LPG substitution alone would represent a meaningful boost to profitability across the company’s olefins and polyolefins chain.

If polymer prices continue to recover while global operating rates remain constrained, the combination of lower feedstock costs and stronger product prices could create a powerful margin expansion cycle for the Brazilian producer.

For investors and industry observers, Braskem’s strategy illustrates a broader trend across the petrochemical sector: companies are increasingly focused on feedstock flexibility, logistics optimization, and structural cost advantages as they prepare for the next upcycle in global polymer demand.

Takeaway

I continue to increase my position in Braskem, as the Alagoas situation is expected to conclude in 2026, clearing a key operational uncertainty.

Source: Braskem

Petrobras has signaled potential financial support, contingent on the completion of the IG4 transaction, which adds another layer of security for Braskem’s balance sheet.

Polymer prices are trending higher, providing a tailwind for margins, while closures in Asian and Middle Eastern plants suggest potential supply tightness and likely catalyst replacements, further supporting global pricing.

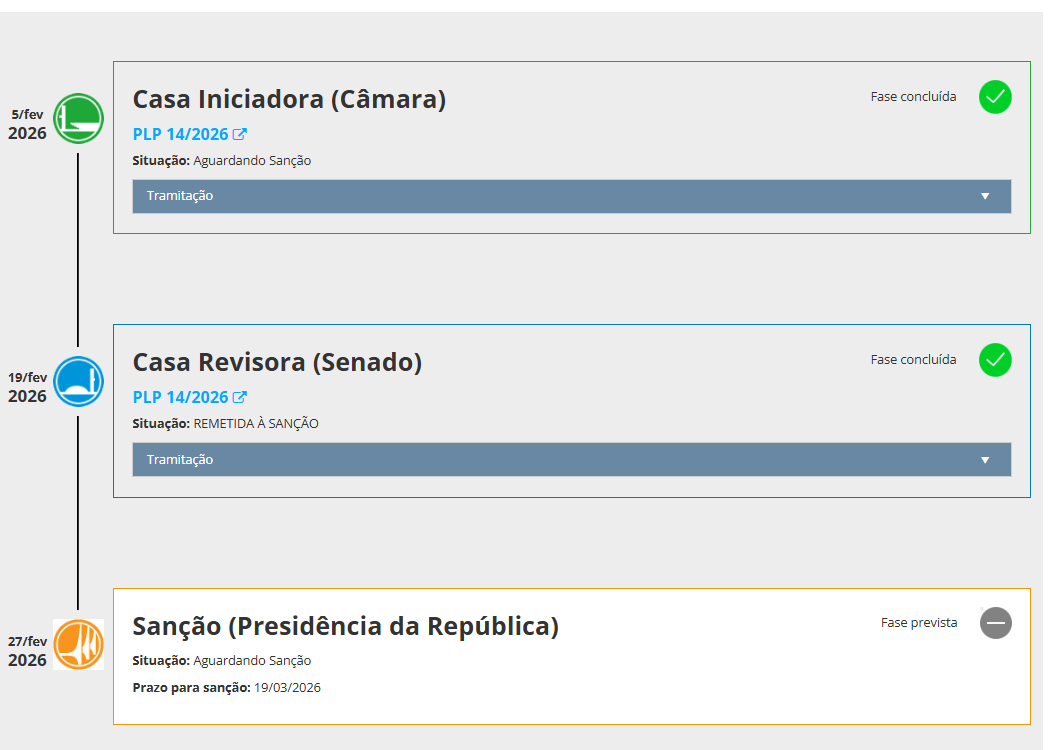

Oversupply in the market is steadily declining, reinforcing the positive demand-supply dynamics. Additionally, the imminent signing of Projeto de Lei Complementar Nº 14/2026 by President Lula should unlock further regulatory clarity and strategic flexibility for the company.

Source: Congresso Nacional

Taken together, these factors point to an improving operating environment and a clearer path toward profitability.

Braskem appears well-positioned to benefit from tightening supply, supportive policy measures, and rising polymer prices, making it an attractive buy in the current cycle.

Drop a like if you’d buy too, and hit follow to track every move!