Braskem’s Alagoas Provisions: Signs of Risk Normalization and Operational Efficiency

When analyzing Braskem’s financial and operational performance, one of the most telling indicators is how the company manages risk and liabilities in its Alagoas operations.

In this article, I take a detailed look at historical trends in provisions, examine the efficiency of settlements, and assess the implications for Braskem’s financial health and strategic flexibility.

My goal is to provide investors with a clear picture of risk normalization, operational improvements, and when the company might reach a point of maximum financial efficiency.

Historical Trends and Provisions Dynamics

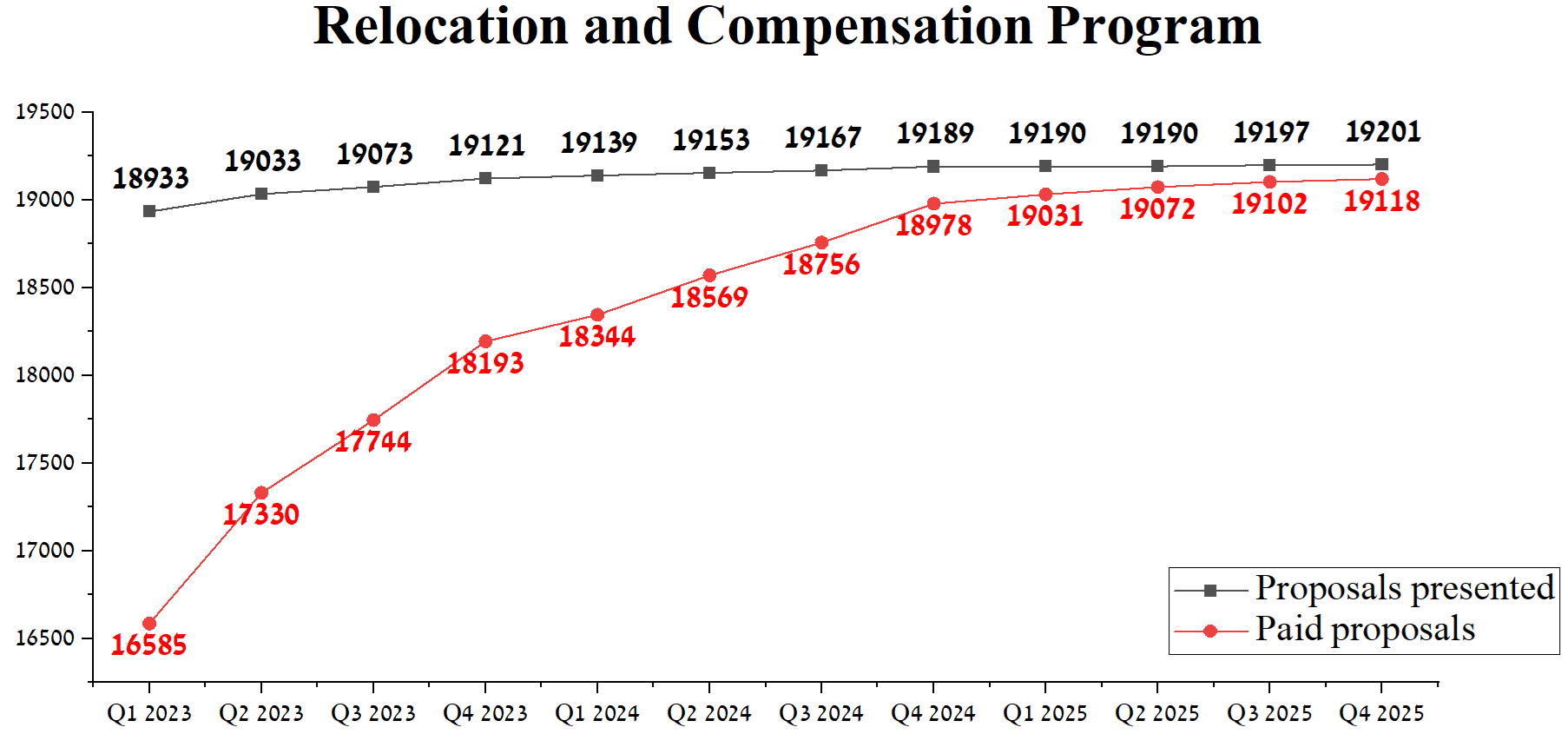

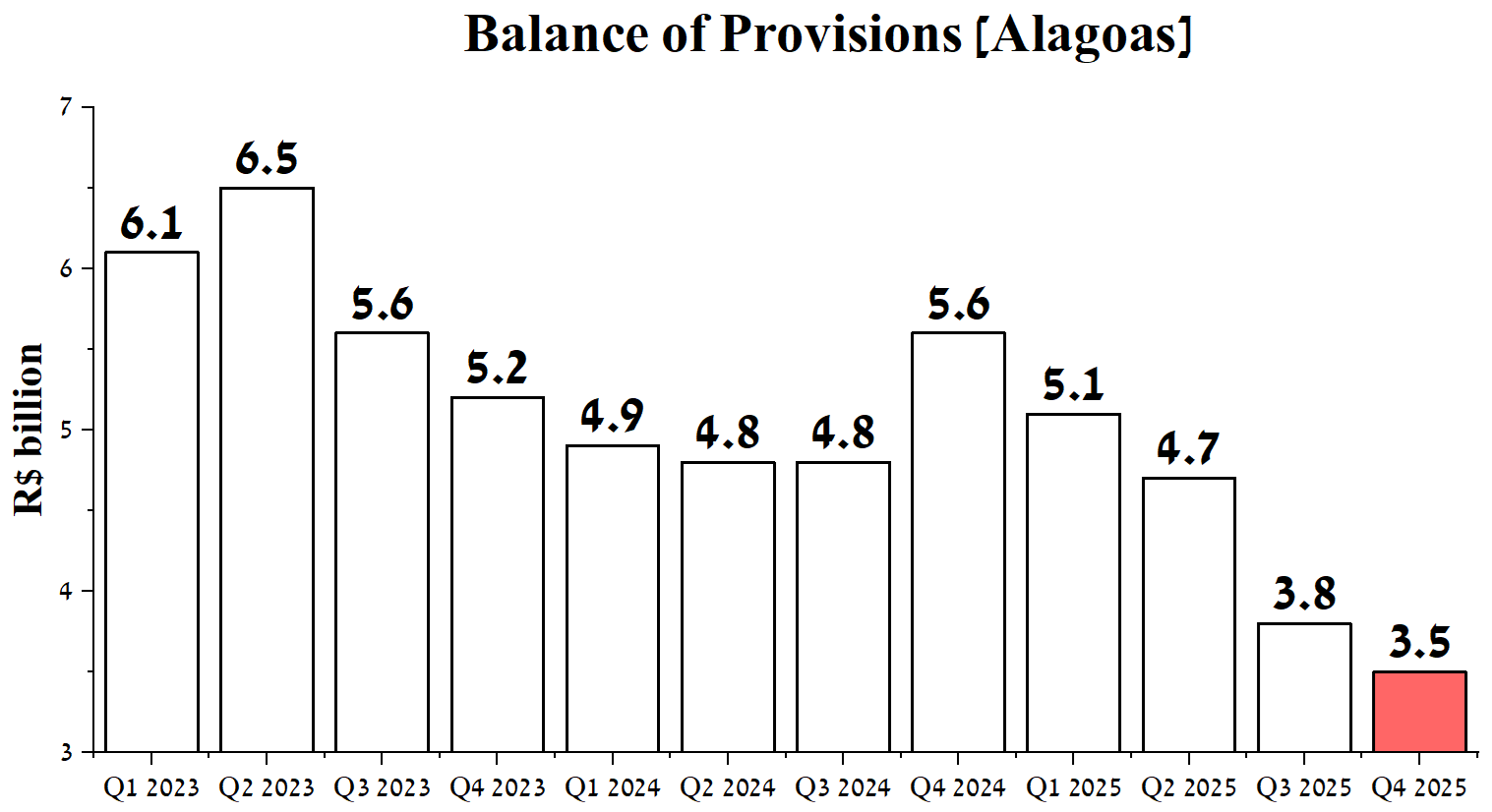

Analyzing Braskem’s Alagoas operations over the past three years, I observe a clear trajectory in the Balance of Provisions that signals how the company manages operational risk and potential liabilities.

From Q1 2023 to Q4 2025, the provision balance decreased from R$6.1 billion to R$3.5 billion, albeit with a notable spike at R$5.6 billion in Q4 2024.

At the same time, the number of proposals presented increased modestly, from 18,933 to 19,201, while paid proposals steadily approached the total, indicating more predictable and efficient settlements.

Source: table was made by ALLKA Research

The Q4 2024 spike is particularly noteworthy.

Based on the company’s operational context, this temporary increase reflects a new recommendation from the specialized technical consultancy hired to conduct studies on the definitive closure of the salt cavities.

Specifically:

An increase was recorded in the provision for filling 11 pressurized cavities with solid material, currently belonging to the Plugging and Pressurization group.

This action follows the evolution of knowledge about the long-term stabilization of the cavities, based on monitoring data collected to date and the need to define the definitive closure of the Mine, as mandated by mining legislation.

The estimated additional provision is approximately R$1.2 billion, related to measures for filling the pressurized cavities, which, if necessary, will begin in 2027 and be executed over several years or decades.

On the Q4 2024 earnings call, Rosana Avolio had this to say.

On the salt cavity closure front, a new recommendation from the technical consultancy hired by the company considers that once the current filling plan has been completed, it is recommended to fill the cavities that are currently pressurized.

To this end, the company increased its provision by R$1.3 billion, of which R$1.2 billion was earmarked for measures to fill in the eleven salt cavities that are currently part of the tamponing and pressurization group with solid material.

In this way, provision is made for actions to ensure that the 35 cavities reach a maintenance-free state in the long term. These actions for definitive closure, in case they be necessary, are scheduled to begin in 2027, with execution over several years or even decades.

This historical view demonstrates that Braskem is not only reactive but also increasingly proactive in managing operational and financial uncertainties.

Efficiency in Settlements and Operational Improvements

From Q1 2025 onward, the trend shifts toward a consistent decline in provisions, reaching a low of R$3.5 billion by Q4 2025, even as proposals presented slightly grow.

Source: table was made by ALLKA Research

This clearly indicates improved efficiency in claims management: paid proposals nearly match total proposals, signaling that Braskem is resolving obligations in a more predictable and structured manner.

I interpret this trend as evidence of several strategic improvements:

Faster claims resolution: Reduced need for precautionary provisions and more accurate liability forecasting.

Enhanced operational processes: Adjustments in Alagoas plants seem to have mitigated recurring incidents that previously contributed to higher provisions.

Optimized cash allocation: Lower and more predictable provisions free up capital, enabling more targeted investments or debt management.

On the Q4 2025 earnings call, management confirmed the progress.

Now with regard to the Alagoas' geological event, we signed an agreement with the state valued at BRL 1.2 billion in payment, of which the vast majority has already been paid.

And so considering the total provisioned amount of BRL 18 billion and the payments that company has already disbursed by the end of 2025, we have a remaining provisioned amount of BRL 3.5 billion to be paid over the coming years, which demonstrates the company's strong commitment and healthy advances in improving the situation after the Alagoas event.

Looking ahead, I see a clear opportunity: if the Balance of Provisions stabilizes below R$4 billion consistently, Braskem will enter a new phase of financial robustness. At this point, the company could redirect resources toward growth initiatives, operational expansion, and efficiency programs without compromising risk coverage.

When Will the Situation Improve Significantly?

Based on the trend, I expect that by mid-2026, Braskem could consistently maintain provisions below R$2.5–2.8 billion, paid proposals would fully track total proposals, and operational efficiencies would be fully reflected in cash flow and working capital.

At that stage, the company will enjoy maximum flexibility to execute strategic plans while minimizing unexpected financial risks.

Conclusion

From my analysis, Braskem’s Alagoas operations are steadily normalizing in terms of risk exposure and operational efficiency. While Q4 2024 highlighted a temporary pressure point due to the salt cavity closure provision, subsequent quarters clearly reflect proactive management and stronger claims handling.

For investors, I focus on three leading indicators:

Balance of Provisions consistently below R$3 billion

Paid proposals closely tracking proposals presented

Management commentary confirming operational and regulatory improvements

If these trends continue, Braskem will likely unlock enhanced cash flow, greater operational predictability, and a solid foundation for sustained growth, ultimately improving investor confidence and strategic flexibility.

Disclaimer

The information provided in this publication is for informational and educational purposes only and should not be construed as financial, investment, legal, or tax advice. The views and opinions expressed are solely those of the author and are based on publicly available information believed to be reliable, but their accuracy and completeness cannot be guaranteed.

Nothing in this publication constitutes a recommendation, solicitation, or offer to buy or sell any securities, commodities, or financial instruments. Readers should conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.

The author may hold positions in companies or assets mentioned in this publication and may change these positions at any time without notice. Past performance and historical trends are not reliable indicators of future results.

By reading this publication, you agree that the author and ALLKA Research shall not be held liable for any direct or indirect losses resulting from the use of the information contained herein.

Nice piece - it’s all about spreads and how they resist (or don’t resist) upward pressure on naptha costs?