Braskem’s Turning Point: How an IG4 Takeover Could Unlock Strategic Renewal

Braskem’s latest earnings call may have underscored the challenges facing the global petrochemical downcycle, but beneath the cautious tone lies a strategic inflection point that could reshape the company’s trajectory.

Market attention has rightly focused on cyclical spreads and utilization rates, but the potential transfer of control from troubled investor Novonor to private equity firm IG4 Capital [with the implicit support of Petrobras] represents a rare opportunity to reset Braskem’s capital structure and governance framework.

Regulatory Structure Still in Play

Now with regard to the change in the company's shareholder situation and controlling structure, the Brazilian CADE has approved. And now in the U.S., the -- their organization still needs to investigate and approve.

My thoughts and implications for Braskem:

From my perspective, while U.S. regulatory approval is still pending, this is a standard step in cross-border M&A. I view it as a manageable hurdle rather than a risk.

Braskem’s compliance and transparency with authorities give me confidence that approval is likely, and once it’s secured, it removes uncertainty around Novonor’s stake, paving the way for potential strategic improvements and faster debt restructuring. This is a step toward stabilizing the company’s shareholder base.

Company Not a Direct Negotiating Party

I'd just like to highlight that Braskem is not party to these discussions or to these negotiations. And when -- and if Braskem is notified, then we will, in turn, notify the market immediately.

My thoughts and implications for Braskem:

I interpret this as a way for Braskem to maintain operational focus while the deal progresses.

This detachment reduces distraction, meaning the company can stay disciplined in its day-to-day operations. At the same time, a successful transaction could bring in a shareholder aligned with growth and stability, enhancing Braskem’s long-term strategic flexibility.

Shareholder Change Could Accelerate Debt Restructuring

Now with Novonor and the Shining (sic) [ Shine I ] credit funds, including with any related topics will all be announced to the market if and when they arise.

My thoughts and implications for Braskem:

I see the potential exit of Novonor as a major positive. Removing a problematic investor opens the door for more aggressive and efficient debt restructuring, particularly with Petrobras.

Shareholder Discussions and Regulatory Review

As we've mentioned at the beginning of the call, there was public information that was published by the CADE and was materialized by the U.S. in the beginning of March with regard to the antitrust and final negotiations with the shareholders.

So this is a topic that for us, there is our due diligence, the analysis that's done by potential investors.

This remains ongoing here at the company, and we continue to respond to these requests in a timely manner. So -- and to send them to the market so that the market remains apprised in a timely manner as well.

My thoughts and implications for Braskem:

In my opinion, even though Braskem is not directly involved in these shareholder discussions or negotiations, I am encouraged by how the company is actively monitoring the situation and prepared to notify the market promptly once informed.

By staying responsive to inquiries and keeping the market updated, I believe Braskem is positioning itself to advance its strategic and financial plans more smoothly once these external steps are resolved.

Petrobras as a Catalyst — Not a Roadblock

So Petrobras is notified in a very timely manner of everything happening at Braskem. In addition, the Petrobras Board has direct access to the Braskem Board. And we talk every week, multiple times a week.

So Petrobras is fully aware of the Braskem situation and the extremely negative petrochemical cycle. They are also enormously interested in the stake that they hold here at the company and the interest they have at the company.

My thoughts and implications for Braskem:

Crucially, Petrobras’ receptiveness to IG4’s proposal (as reported by Reuters) reinforces the viability of the transaction and suggests alignment among major stakeholders.

For Braskem, a supportive Petrobras reduces the likelihood of drawn‑out shareholder conflict and increases the odds of a smoother transition — potentially unlocking better financing terms, given Petrobras’ own strategic interest in the viability of its largest petrochemical partner.

IG4 Momentum Continues

Rosana Avolio said the following.

Could there be any type of support from Petrobras to Braskem considering that the transaction with IG4 has been approved and the new shareholders' agreement is likely to be signed briefly.

Felipe Montoro Jens answered.

And with regard to the relevance between Petrobras and Braskem, we continue to work to develop future improvements and commercial conditions. Of course, respecting both parties so that both parties can reach an agreement that is fruitful for both companies.

I believe that these discussions remain ongoing in parallel. They've always remained ongoing regardless of the -- any potential shareholder situation.

My thoughts and implications for Braskem:

I interpret this as a possible signal that, even without formal commitments, management may be hinting at a supportive stance from Petrobras over time.

I also find it notable how the question itself was framed-highlighting that the IG4 transaction has been approved and that a new shareholders’ agreement is “likely to be signed briefly.”

To me, this implicitly points to a near-term timeline for the deal, and management’s willingness to engage with the question may indicate that progress is indeed advancing toward completion.

Conclusion

In my view, the potential transition of control to IG4 Capital represents a meaningful turning point for Braskem. Beyond the operational challenges highlighted in the call, this transaction could mark the beginning of a structural shift — away from the overhang of Novonor and toward a more flexible and investment-driven ownership structure.

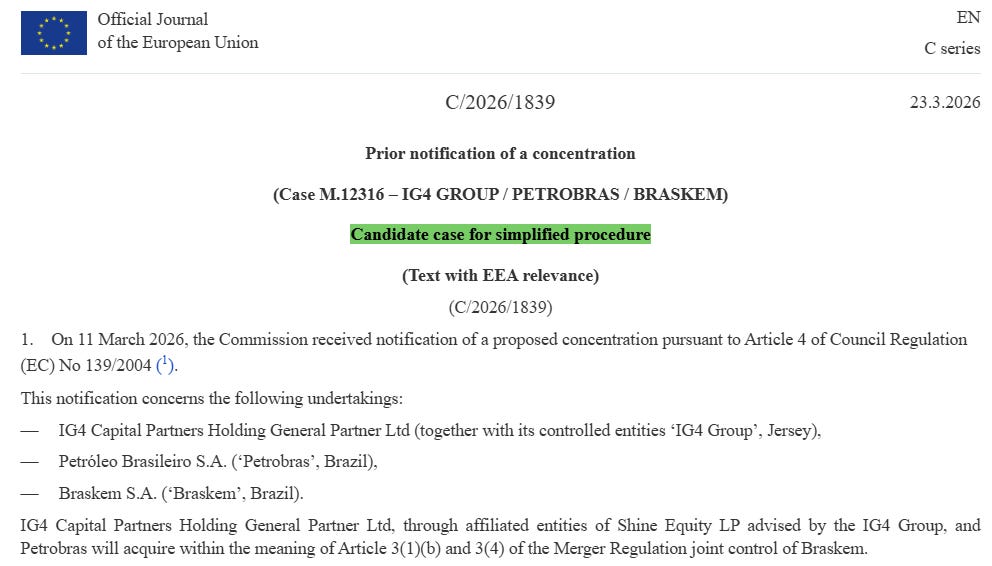

What reinforces my constructive view is the broader regulatory backdrop. The European Commission’s filing — C/2026/1839 (Case M.12316 – IG4 Group / Petrobras / Braskem) — has been classified as a candidate for simplified procedure, which typically implies limited competition concerns and a more streamlined review process.

Source: EUR-Lex: EU law

Importantly, the notification has already been submitted, and the review timeline is progressing toward its deadline, suggesting that regulatory clarity may arrive in the near term.

Taken together, I see a setup where multiple pieces are gradually aligning: regulatory approvals advancing, due diligence ongoing, and continued engagement with Petrobras.

If the process concludes as expected, Braskem could emerge with improved governance, stronger strategic alignment, and a clearer path toward addressing its balance sheet — all of which have the potential to unlock a re-rating over time.

Disclaimer

The information provided in this publication is for informational and educational purposes only and should not be construed as financial, investment, legal, or tax advice. The views and opinions expressed are solely those of the author and are based on publicly available information believed to be reliable, but their accuracy and completeness cannot be guaranteed.

Nothing in this publication constitutes a recommendation, solicitation, or offer to buy or sell any securities, commodities, or financial instruments. Readers should conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.

The author may hold positions in companies or assets mentioned in this publication and may change these positions at any time without notice. Past performance and historical trends are not reliable indicators of future results.

By reading this publication, you agree that the author and ALLKA Research shall not be held liable for any direct or indirect losses resulting from the use of the information contained herein.

The case for Braskem as a "turning point" story is a great study in how a change in controlling ownership can unlock value in a distressed asset, especially when moving from a complex conglomerate structure to a more specialized private equity approach like IG4’s. It highlights that in the petrochemical industry, the "governance discount" is often as significant as the commodity cycle itself.

Given the environmental liabilities in Alagoas and the cyclical nature of polyethylene spreads, do you see the IG4 involvement primarily as a catalyst for a cleaner exit via a sale to a strategic buyer like Adnoc, or is the core of the thesis built on a long-term operational turnaround that can withstand a potential downturn in global demand?