Brazil’s PLP 14/2026: A Temporary Fix That Could Add Up to $200M to Braskem’s EBITDA

Brazil is poised to approve PLP 14/2026, with the bill likely to be signed into law imminently, potentially today. In my view, this is not a broad structural reform but a targeted fiscal measure aimed at preventing a sharp deterioration in petrochemical margins in 2026 for domestic players, notably Braskem.

Source: Congresso Nacional

Mechanics of the Bill

At its core, PLP 14/2026 is a stopgap mechanism designed to prevent a sharp deterioration in industry economics during 2026, following the discontinuation of the previous REIQ tax regime.

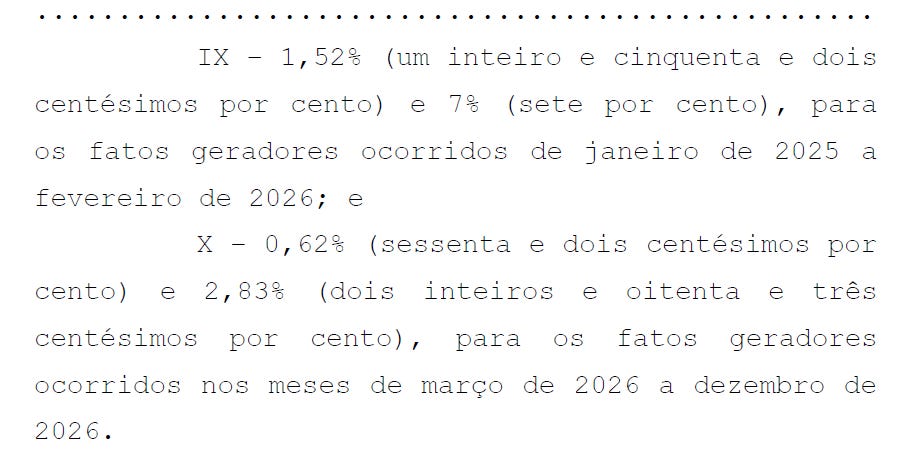

The legislation reduces PIS/COFINS taxes on key petrochemical feedstocks.

Effective rates drop from 8.52% during January 2025 through February 2026 to 3.45% from March through December 2026, implying a 507 basis point reduction on critical inputs, including natural gas, naphtha derivatives, and core intermediates such as phenol, acetone, and purified terephthalic acid.

Source: Congresso Nacional

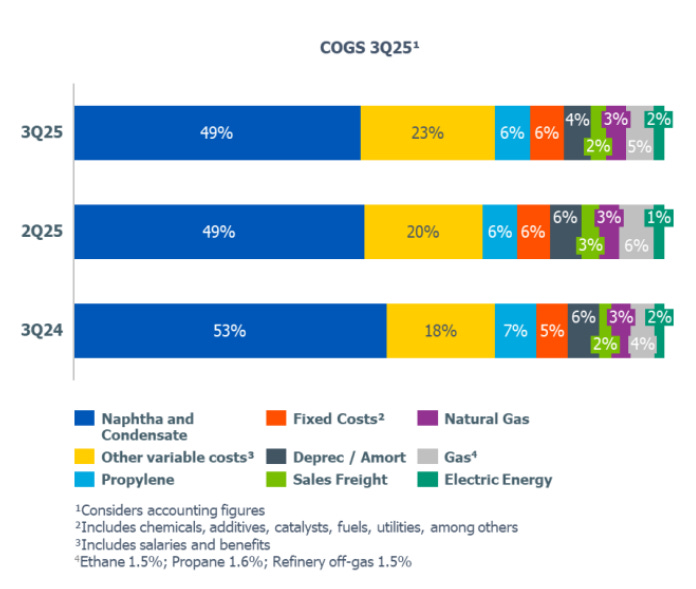

Feedstock costs typically represent 60%–70% of Braskem’s cost of goods sold, meaning this relief could significantly compress cash costs per ton of ethylene and polyethylene.

Source: Braskem

Potential Financial Impact

A back-of-the-envelope sensitivity analysis, assuming $8 billion–$10 billion of annual feedstock exposure, suggests that a 5% reduction in costs could theoretically boost EBITDA by $320 million–$400 million.

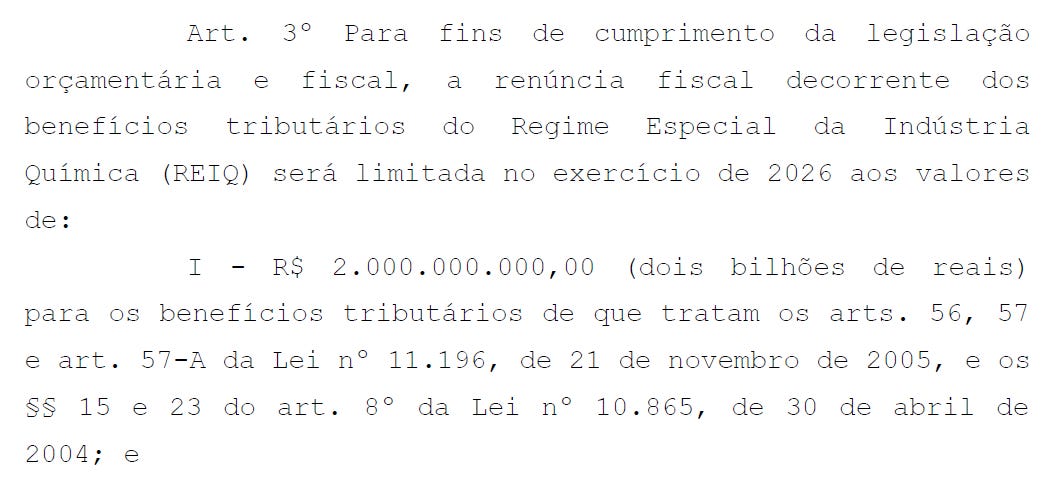

This aligns with the widely cited $300 million–$380 million range. However, the bill’s hard fiscal cap limits total sector relief to R$2 billion (≈$400 million) in 2026, which tempers the headline potential.

Source: Congresso Nacional

Considering Braskem’s share of domestic production and feedstock usage, I estimate the company could realistically capture 30%–50% of the total pool.

This translates into an actionable EBITDA uplift of $120 million–$200 million, representing a 25%–40% increase relative to the current run-rate, depending on macro and cycle conditions.

Conclusion: A Capped Fiscal Bridge

PLP 14/2026 effectively lowers feedstock taxation by over 500 basis points but imposes a sector-wide limit of R$2 billion.

For Braskem, this results in a tangible and executable EBITDA boost of $120 million–$200 million. While sufficient to stabilize margins and mitigate downside risk, it does not constitute a structural re-rating catalyst.

The trajectory of policy support beyond 2026 will be crucial for shaping Braskem’s longer-term investment case.

In parallel to global economic developments, geopolitical tensions in the Middle East have sharply escalated. Israel reportedly conducted a significant strike on Iran’s critical South Pars gas field — the world’s largest — leading to explosions and disruptions in Iranian energy infrastructure, and Tehran has since launched retaliatory missile strikes that caused damage to energy facilities in neighboring Qatar.

Gulf states have condemned the attacks, heightening regional uncertainty and driving volatility in global energy markets.

Disclaimer

The information provided in this publication is for informational and educational purposes only and should not be construed as financial, investment, legal, or tax advice. The views and opinions expressed are solely those of the author and are based on publicly available information believed to be reliable, but their accuracy and completeness cannot be guaranteed.

Nothing in this publication constitutes a recommendation, solicitation, or offer to buy or sell any securities, commodities, or financial instruments. Readers should conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.

The author may hold positions in companies or assets mentioned in this publication and may change these positions at any time without notice. Past performance and historical trends are not reliable indicators of future results.

By reading this publication, you agree that the author and ALLKA Research shall not be held liable for any direct or indirect losses resulting from the use of the information contained herein.