Investors Still Think Braskem Runs on Naphtha. It Doesn’t.

I think the market is getting Braskem wrong.

The dominant narrative still frames the company as a naphtha-heavy petrochemical producer — effectively tethered to oil prices and structurally disadvantaged versus gas-based competitors. That view might have been accurate 15 years ago. Today, it looks increasingly disconnected from reality.

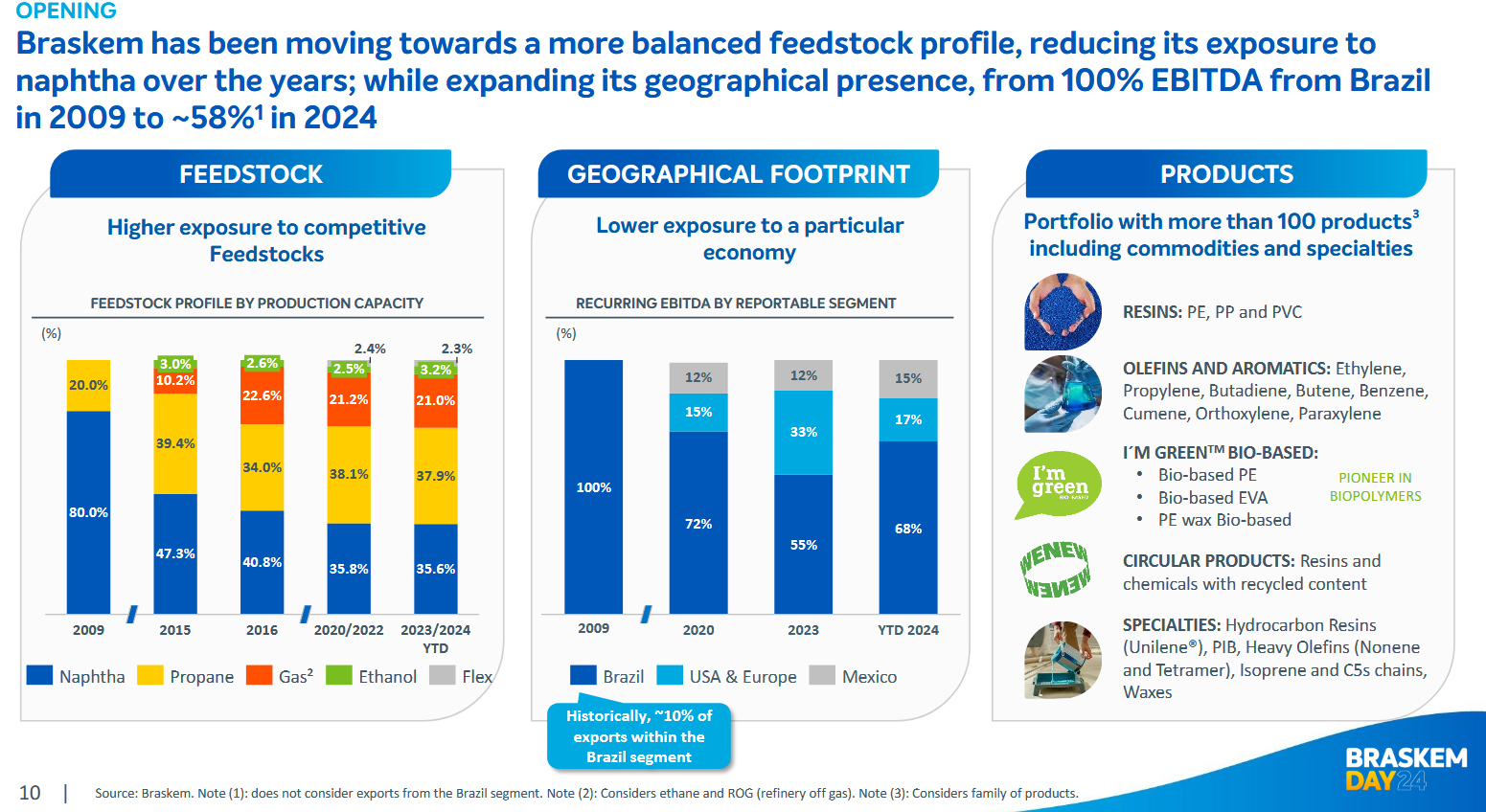

Since 2009, Braskem has been quietly executing a structural shift in its feedstock mix. Back then, roughly 80% of its production capacity relied on naphtha. Over time, that exposure has been steadily reduced to the mid-30% range. The gap has been filled by propane, gas-based inputs, ethanol and flexible feedstocks.

Source: Braskem

In other words, the company many investors still view as an oil-linked petrochemical player has been systematically moving toward gas.

That distinction matters more than ever in the current commodity cycle. Natural gas prices — particularly across the Americas — remain significantly cheaper than oil-derived naphtha. For petrochemical producers, feedstock costs are often the single most important determinant of margins. When gas trades at a structural discount to oil, gas-based producers enjoy a meaningful cost advantage.

Source: Braskem

Braskem’s repositioning effectively brings its economics closer to those of North American chemical producers, whose global competitiveness has long been driven by abundant and relatively cheap gas feedstock.

The strategic backdrop is further strengthened by Braskem’s relationship with Petrobras. The industrial partnership provides access to domestic hydrocarbons and integrated infrastructure, creating supply stability and feedstock flexibility that many international competitors operating in Brazil lack.

Source: Braskem

That integration becomes particularly valuable when feedstock price spreads widen — exactly the environment the industry is experiencing today.