Petrochemicals Enter a New Cycle as Hormuz Disruptions Tighten Global Supply

A combination of geopolitical disruption and structural supply tightening is rapidly reshaping the global petrochemical landscape.

Comments from LyondellBasell highlight how constraints in the Strait of Hormuz are not only limiting exports from the Middle East but also amplifying already low inventory levels and accelerating price increases across polyethylene and polypropylene markets.

Source: LyondellBasell

At the same time, years of capacity rationalization and resilient demand—particularly in the U.S.—suggest that the industry was already approaching an inflection point. The current disruption may now be acting as a catalyst, pushing the sector into the early stages of a new upcycle.

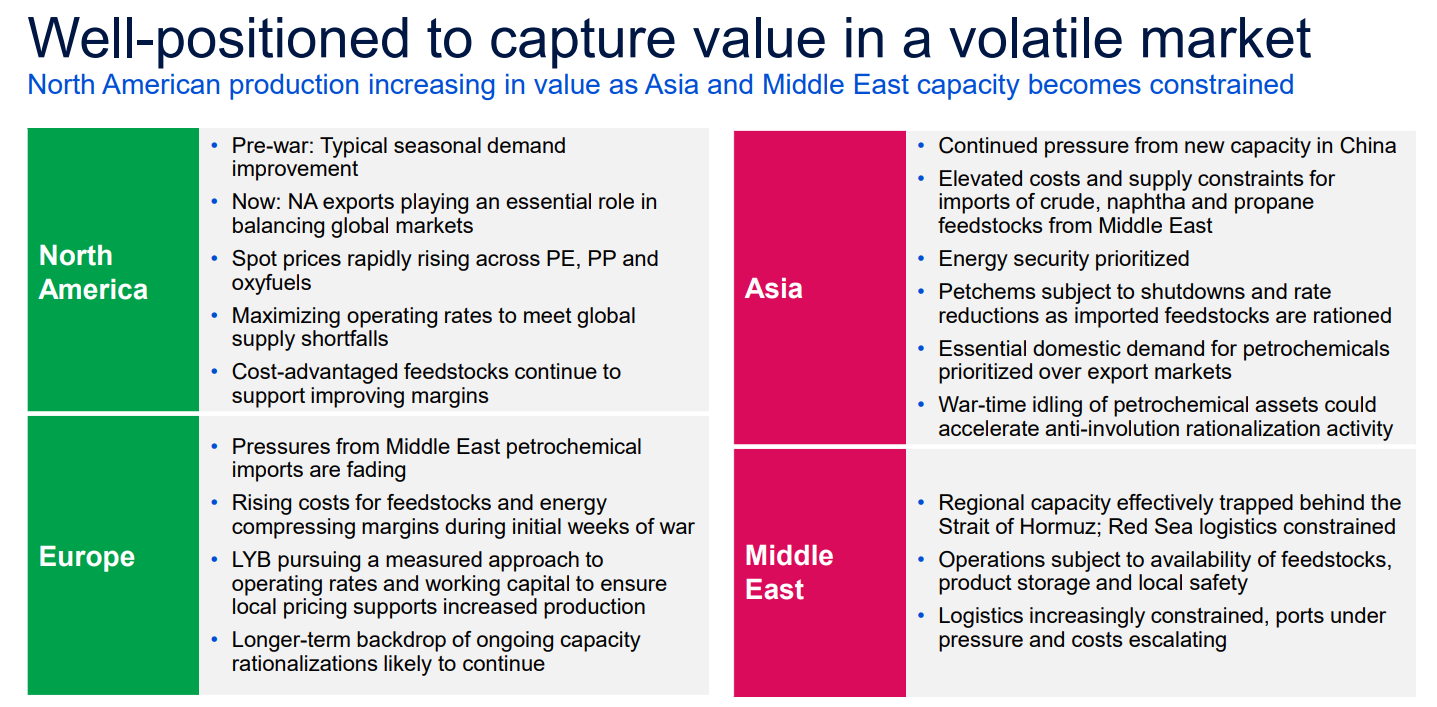

Strait of Hormuz disruption

Comment (call):

And Middle East, of course, the war, the conflict is creating quite a bit of disruptions in the Strait of Hormuz. We'll touch about on some of the capacities and how they're affected but the materials obviously become very, very constrained, both on the material that is trapped as well as the feedstock implications that it has for Asia.

The operating rates, which we'll also touch on, we haven't seen much change actually in terms of operating rates in the Middle East, but they will start to run out of storage if the supply chain doesn't improve fairly quickly here. And the constraints will also -- even after the conflict is resolved, will take a few months to normalize.

My take:

I see this as a major supply shock. For LyondellBasell, this directly supports margins and pricing power. For Braskem, this is even more bullish given its sensitivity to spreads. For the petrochemical industry, this is the kind of disruption that can kickstart a new cycle.

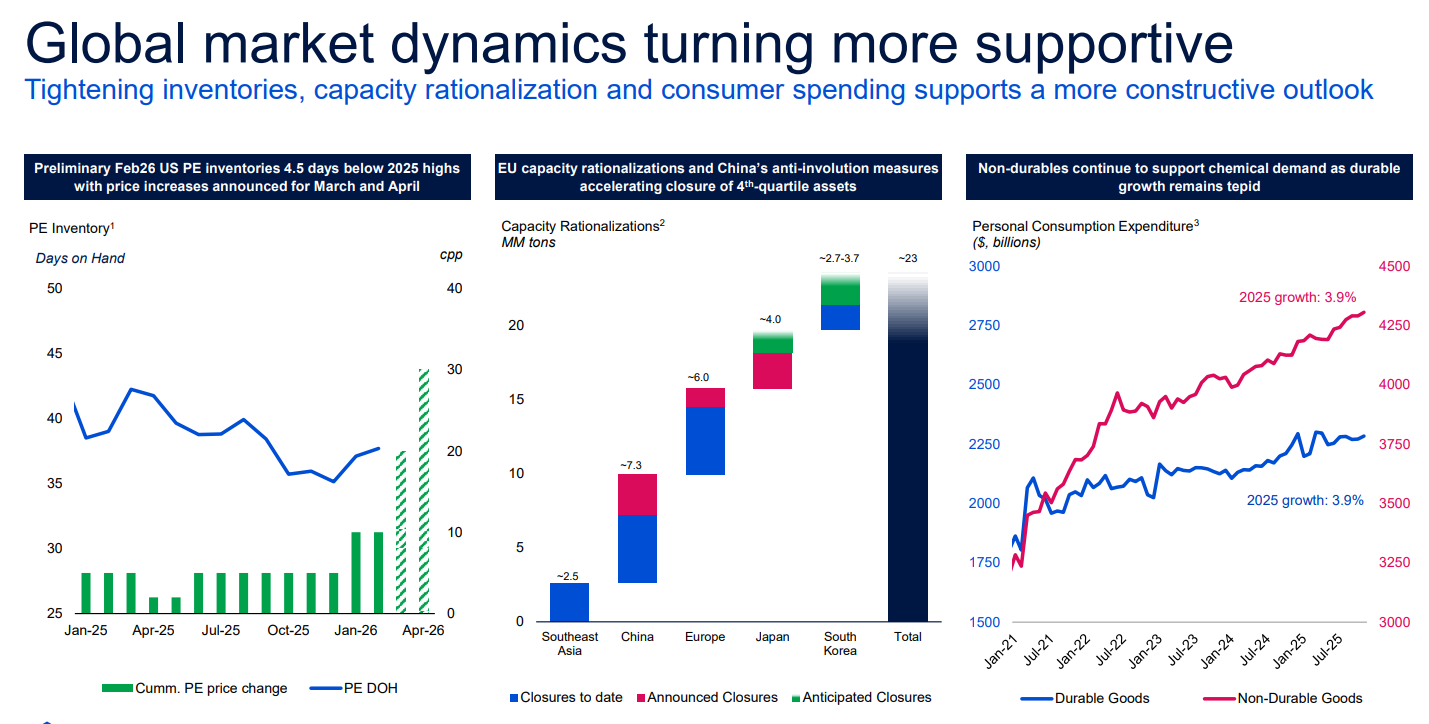

Low PE inventories supporting price increases

Comment (call):

At the very -- on the left-hand side, we have the days -- inventory days for PE. And if you recall, we finished the fourth quarter with inventory days around 37 days PE. This is according to the ACC statistics. This is very low levels. We usually balance when we're about 45 days, which was also very supportive for the January price increase that we got the $0.05 per pound.

Then as you recall, February was flat. And of course, after the conflict, we have nominations for $0.10 per pound for March as well as April with some producers even having nominations of $0.15 per pound. But what we saw also the February statistics just came down, even though utilization rates increased, the inventory days at ACC level are 37.7 versus 37.1.

My take:

I view this as real pricing power, not just expectations. For LyondellBasell, this translates into immediate EBITDA upside. For Braskem, this is critical given its exposure to polyethylene spreads. For the industry, this confirms that we’ve moved out of oversupply conditions.

Structural capacity rationalization

Comment (call):

It's roughly the 23 million metric tons of ethylene capacity that are coming out of the system across the world with an acceleration, I would say, particularly in Europe. We've also seen announcements in Japan, in South Korea and the anti-involution measures that have been announced in China.

There's still more to come on the net, I would say, from now until 2030, roughly 13 million metric tons, which we'll also talk about this, what's going on in the Middle East right now.

Source: LyondellBasell

My take:

I see this as a structural bull case. For LyondellBasell, this improves long-term utilization and margins. For Braskem, this strengthens its positioning in a tighter global market. For the industry, this marks a shift toward supply discipline.

Demand remains resilient

Comment (call):

Demand in the U.S. hasn't really come down, continues to be fairly healthy at around the 2% or 3%, close to 4% here in 2025, and that gives us hope. Eventually, the cycle will have to come back, right, the durables that we bought during COVID, the replacement will have to come after 5 or 6 years.

And that's what we're starting to see, which, as I mentioned at the beginning, combined with good PMI numbers that we saw at the beginning of the year was giving us hope even before the conflict started that there could be light at the end of the tunnel for the PE cycle and PP as well.

My take:

I see demand holding up better than expected. For LyondellBasell, this supports high operating rates. For Braskem, this amplifies the impact of tighter supply. For the industry, this suggests the upcycle is supported by both demand and supply dynamics.

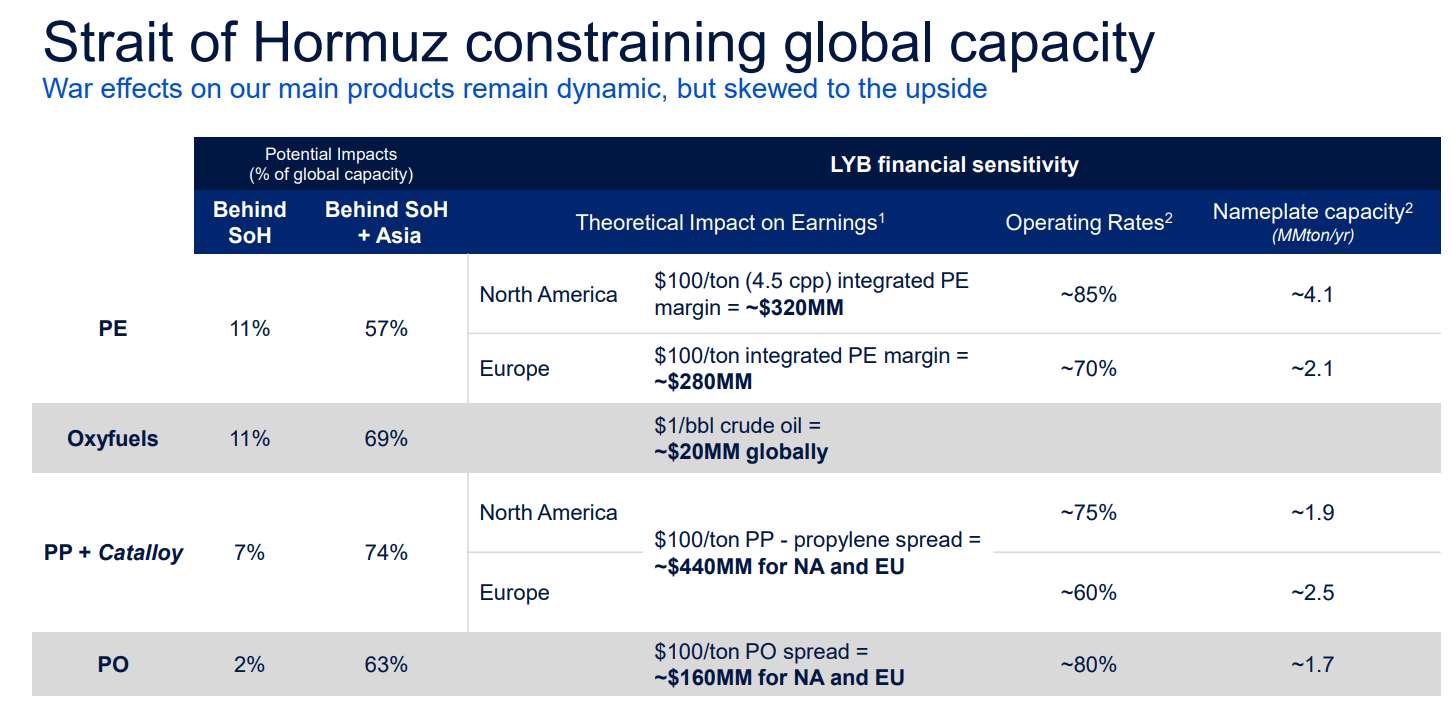

Strong operating leverage to PE pricing

Comment (call):

Here, the 57% that you see here on the slide, that's the overall sort of PE that is touched, not necessarily the 30% that I just mentioned. But you can see how leveraging it is in North America, $100 per ton increase is $320 million of EBITDA for us.

And if you recall, our operating rates of 85%, which we have listed here, we still have room to increase by 5% to 10%, which is obviously very supportive for us. In Europe, $100 per ton increase, as you can see there, translates a little bit less is $280 million for EBITDA annualized, but our operating rates were much lower. So we have the room to grow by, call it, 15% to 20% more. So there's significant upside.

Source: LyondellBasell

My take:

I see extreme operating leverage here. For LyondellBasell, even small price increases drive significant earnings growth. For Braskem, the upside is even more pronounced due to historically low margins. For the industry, this explains why equities can react sharply to pricing.

Logistics disruption + PP upside

Comment (call):

And in the case of polypropylene, which you know is the -- we call it the sleeping giant for LyondellBasell, which we haven't been able to push much spread increase over the past few years, you can see how leveraging this is in terms of $100 per ton. It's roughly $440 million for EBITDA annualized for North America and Europe.

And as we see now throughout the world that it's more difficult to ship propane, you see PDH rates across the globe coming down. I think we've seen rates in Asia even in the mid-50s, which is quite low. And obviously, the material from the Middle East is tracked in the region.

My take:

I see this as a powerful regional dislocation. For LyondellBasell, North America becomes a key export winner. For Braskem, tighter global trade flows improve pricing dynamics. For the petrochemical industry, this fragmentation is highly supportive for margins.

Bottom line

I see this call as confirmation that the cycle was already improving, and the conflict is accelerating it significantly. Pricing power is back, inventories are low, and supply is tightening.

For me, this looks like the early stage of a new upcycle — with LyondellBasell and Braskem as key beneficiaries.