Global plastics prices are sending a clear signal: supply-chain fragility is back.

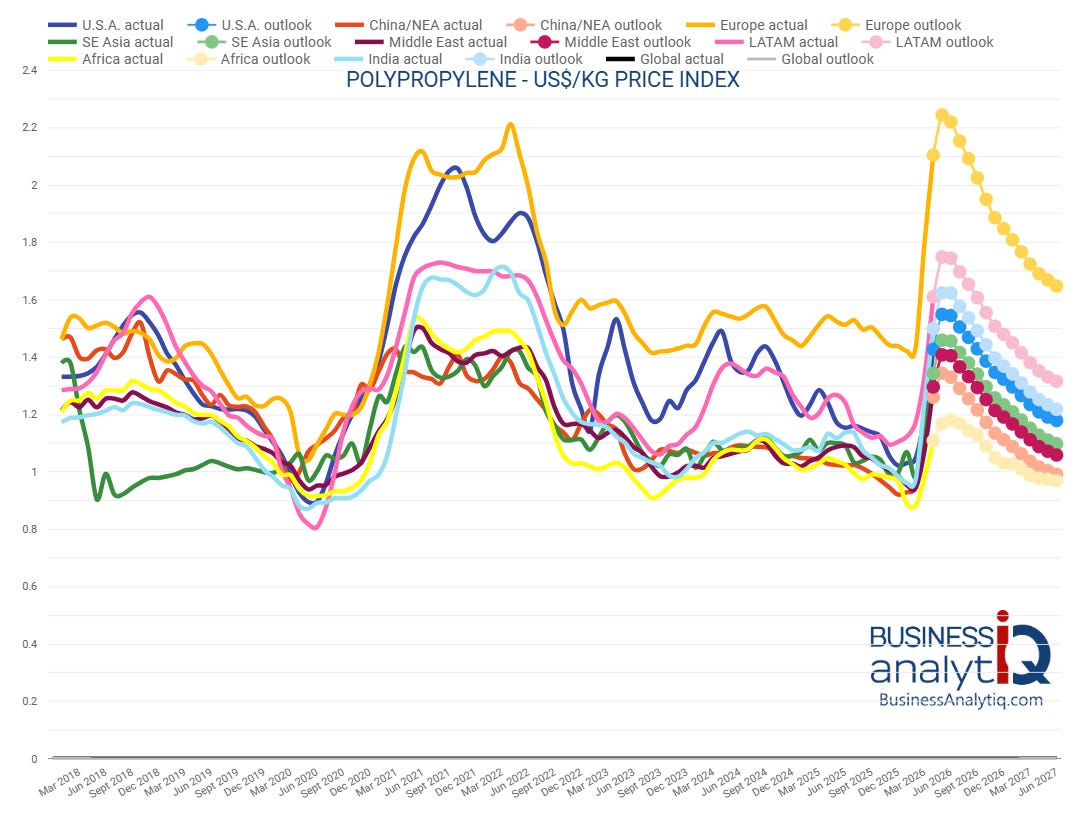

Fresh data from BusinessAnalytIQ’s regional price indices show Latin America (LATAM) polyethylene and polypropylene prices have climbed all the way back to their 2021 pandemic peaks — the highest levels recorded during the COVID-19 supply shock.

Both PE and PP in LATAM are once again trading at those historic tops, reflecting tight regional availability and strong downstream demand recovery.

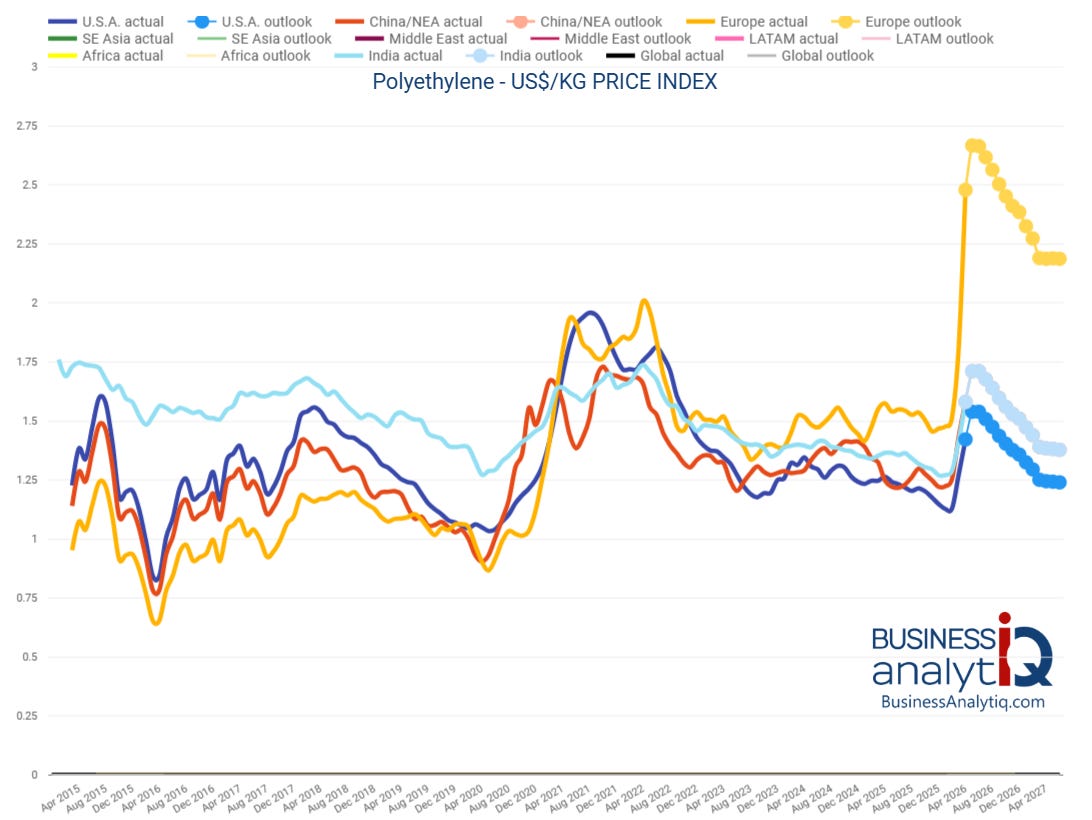

The standout move, however, is in Europe’s polyethylene market.

After trading in the $1.4–1.6/kg range through most of 2024, European PE has nearly doubled relative to typical COVID-era pricing levels, surging above $2.65/kg in the latest actual data before the outlook begins to ease.

Source: Business Analytiq

That is one of the sharpest regional spikes seen in the entire 2015–2027 series and leaves Europe trading at a substantial premium to the U.S., China/NEA, and Southeast Asia.

Polypropylene shows parallel tension.

Europe again leads the upside with a pronounced 2025 spike, while LATAM has matched its own 2021 highs. Most other regions — including the U.S., India, and Africa — remain well below those pandemic-era ceilings, underscoring a highly fragmented global market.

Business Analytiq

Forward curves in both charts point to gradual moderation through 2026–2027, yet the near-term surge highlights lingering vulnerabilities: energy costs in Europe, logistical bottlenecks, and shifting trade flows are once again dictating price action.

Bottom line: the plastics complex is flashing the same regional divergences that defined the 2020–2021 volatility.

For producers, converters, and commodity traders, the message is unmistakable — LATAM is back at COVID highs, Europe’s PE is pricing in a new stress premium, and the outlook remains anything but smooth.

Makes a lot of sense. 👍

Does this mean that BAK is no longer in trouble?