Polymer Prices Surge as Hormuz Risks Shake Global Petrochemicals

Polymer prices are beginning to react sharply to the growing geopolitical shock in the petrochemical supply chain.

On March 16, 2026, polypropylene in China rose to 8,755 CNY/T, while polyethylene reached 8,570 CNY/T.

Source: TRADING ECONOMICS

Over the past month alone, polypropylene prices have surged 30.6%, and polyethylene has climbed 26.3%, marking one of the fastest short-term increases since the post-COVID commodity cycle.

Source: TRADING ECONOMICS

At the same time, polyvinyl chloride (PVC) rose to 5,914 CNY/T, reflecting tightening supply across the vinyl chain as producers begin to react to rising feedstock costs.

Source: TRADING ECONOMICS

The key catalyst behind this move is the growing disruption across global petrochemical logistics. Escalating tensions around the Strait of Hormuz and the wider Middle East conflict have already forced shipping companies to reroute vessels, apply war-risk premiums, and reconsider cargo movements.

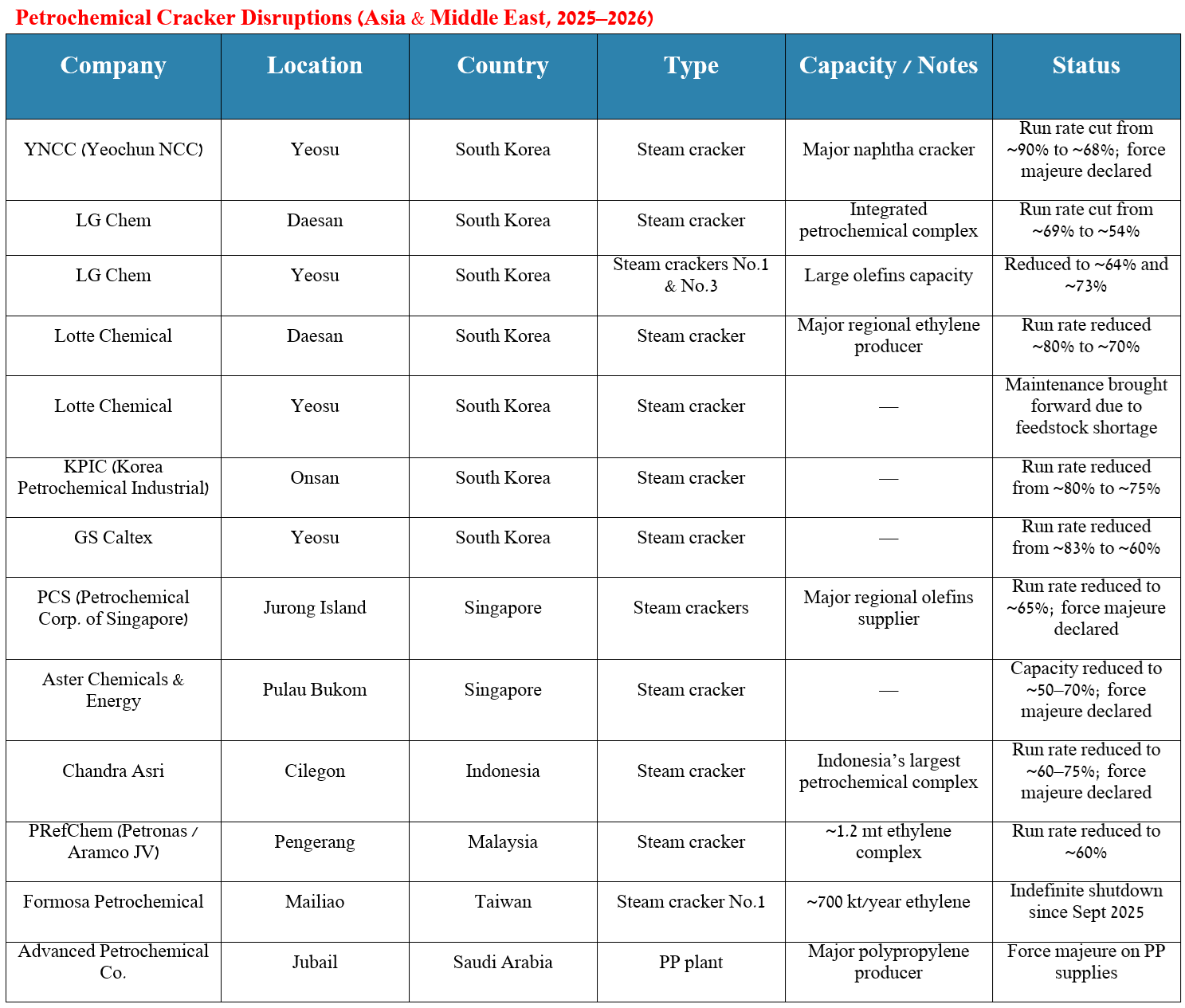

Several Asian petrochemical producers have declared force majeure, while others have reduced operating rates due to uncertainty around feedstock availability and freight costs.

Source: table was made by Author

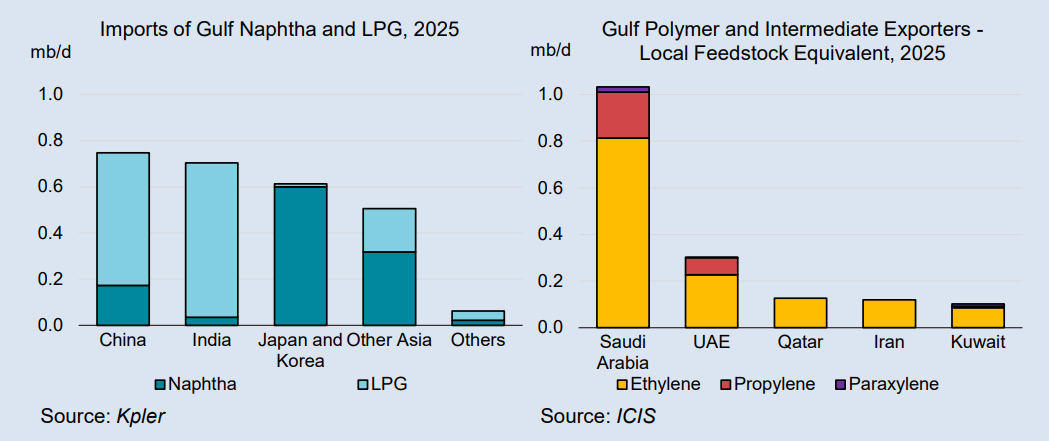

According to the International Energy Agency, the Gulf region plays a disproportionately large role in global petrochemical supply due to its massive production of feedstocks and downstream chemical products.

A significant share of these volumes is exported through the Strait of Hormuz via oil tankers, LPG carriers, and container vessels transporting petrochemical derivatives. In 2025, total shipments from the Gulf exceeded 4 million barrels per day of oil products and petrochemical feedstock equivalents, representing around one-quarter of the global petrochemicals market.

Because such a large share of supply is concentrated in this region, any prolonged disruption to flows through the Strait of Hormuz could have significant consequences for polymer markets worldwide.

Source: IEA

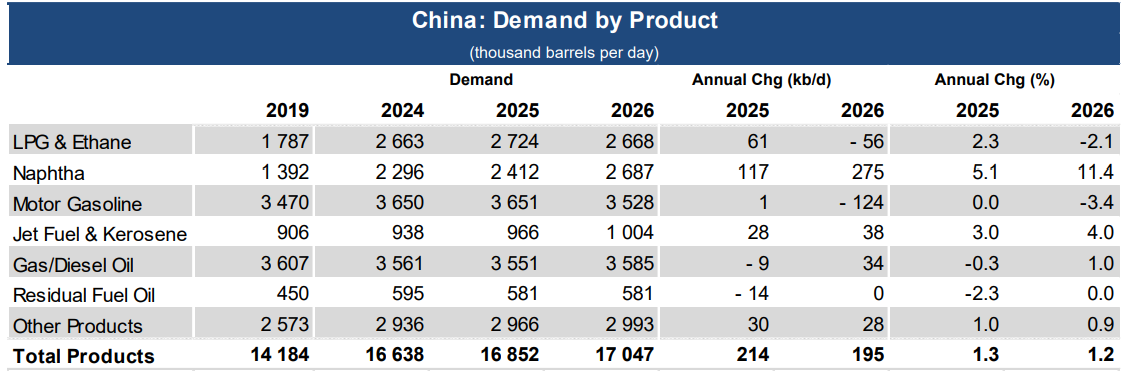

The impact would likely be felt most strongly in Asia, where petrochemical producers and manufacturing industries are deeply integrated with Gulf feedstock suppliers.

A decline in polymer exports from the Middle East could also force Chinese steam crackers to increase naphtha utilization in order to maintain sufficient domestic polymer supply for the country’s manufacturing sector.

Source: IEA

In short, the polymer market may be entering the first stage of a new petrochemical upcycle — driven not by demand alone, but by geopolitical disruption and supply constraints across the global energy and chemical system.

If tensions in the Middle East persist and force majeure declarations continue to spread, the current rally in polymer prices may only be the beginning.

Disclaimer

The information provided in this publication is for informational and educational purposes only and should not be construed as financial, investment, legal, or tax advice. The views and opinions expressed are solely those of the author and are based on publicly available information believed to be reliable, but their accuracy and completeness cannot be guaranteed.

Nothing in this publication constitutes a recommendation, solicitation, or offer to buy or sell any securities, commodities, or financial instruments. Readers should conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.

The author may hold positions in companies or assets mentioned in this publication and may change these positions at any time without notice. Past performance and historical trends are not reliable indicators of future results.

By reading this publication, you agree that the author and ALLKA Research shall not be held liable for any direct or indirect losses resulting from the use of the information contained herein.